SURPRISE INFLATION

The current wave of global inflation, not witnessed for three decades, is causing socio-economic havoc. EPISODE #122

Dear Reader,

A very Happy Monday to you.

Last week the International Monetary Fund released its latest Fiscal Monitor at its Spring meetings in Washington DC. The document, released twice a year, is an overview of the latest developments in public finance and assessment of their fiscal implications.

The latest issue puts the spotlight on rampant inflation which has ravaged the world for the last two years. Worse, one can expect some relief only from next year.

The IMF says this ‘surprise inflation’ needs a strong policy response. This is because rising prices always effect a redistribution of incomes, with the worst affected being those at the bottom of the pyramid. So this week I explore surprise inflation.

Spring is in the air and most of India is in bloom. Nothing to beat the beauty of Kashmir though. The cover picture this year is from the Tulip gardens in Srinagar. It has been taken by Balesh Kumar and generously shared for use. Thank you Balesh.

A big shoutout to Balesh, Gautam, Ranjini, Aashish, Premasundaran and Vandana for your informed responses, kind appreciation and amplification of last week’s column. Once again, grateful for the conversation initiated by all you readers. Gratitude also to all those who responded on Twitter and Linkedin. Reader participation and amplification is key to growing this newsletter community. And, many thanks to readers who hit the like button😊.

THE INFLATION THREAT

It was some three decades ago that the world saw such elevated levels of inflation and for such a prolonged period—it has been two years and the world is still counting its unfortunate tryst with inflation.

The thing is that this bout of inflation occurred all of a sudden. It started with the covid-19 pandemic, which dislocated global supply chains. A bad situation took a turn for the worse with the onset of the Russia-Ukraine conflict—shutting down the world’s granary.

Burgeoning energy and food prices ran rampant, resulting in extremely high and prolonged period of inflation. The International Monetary Fund (IMF) has a moniker for this: Surprise Inflation.

It is the theme of the latest Fiscal Monitor released at the just concluded Spring meetings of the IMF and the World Bank in Washington DC.

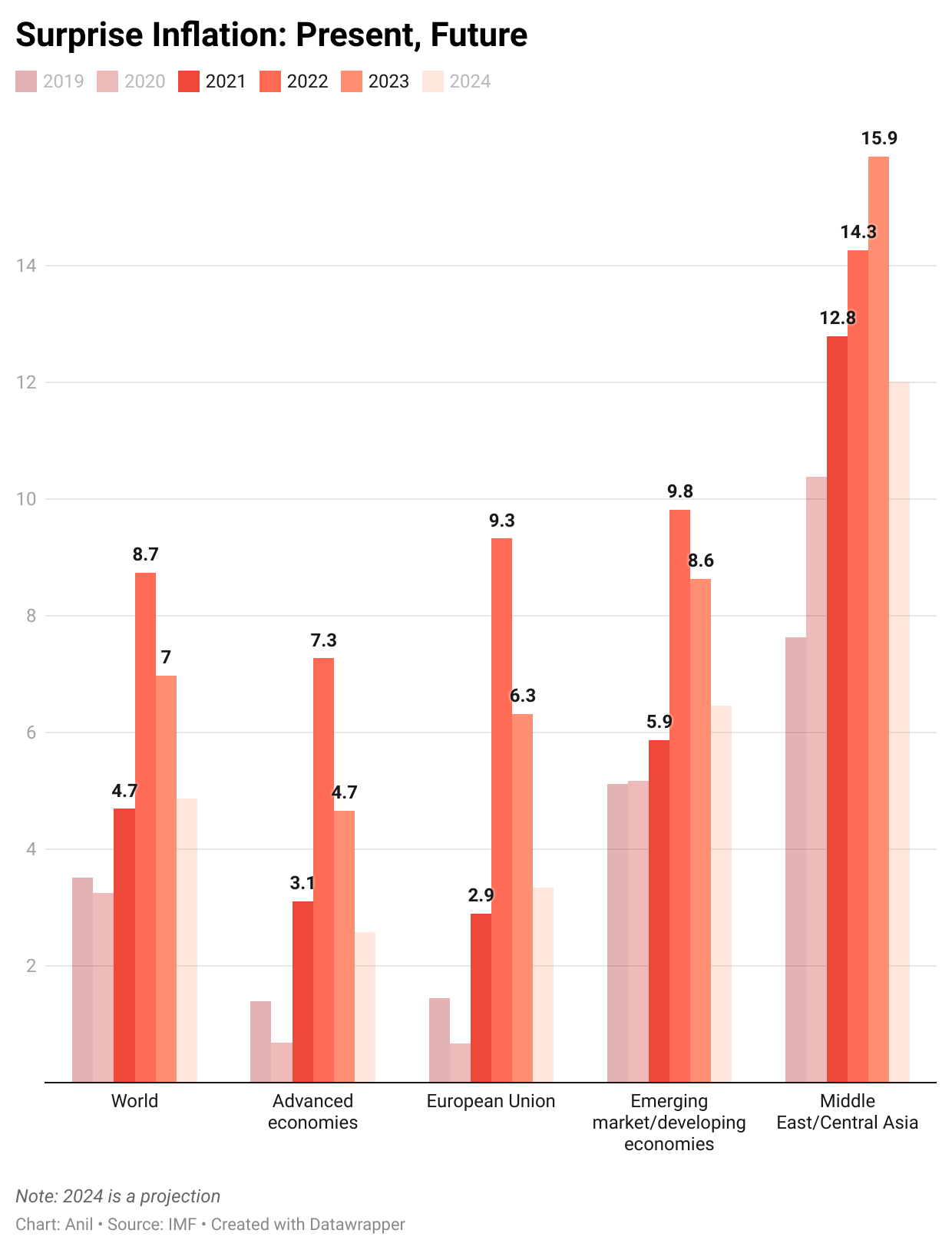

The idea will become clear once you peruse the graphic below. I sourced the data from the IMF data base. Notice, how inflation spurts from 2021.

It is clear that average world inflation surged from 4.7% in 2021 to 8.7% in 2022. The IMF forecasts that it will average 7% this year; it will drop next year, but still remain above the levels that prevailed in 2021.

The challenge is that no region or grouping has been spared. The advanced economies witnessed more than doubling of inflation in just two years. It trebled in the European Union and almost doubled for emerging markets/developing countries. Most worrying were the trends for the Middle East/Central Asia where inflation is accelerating in double digits.

And then you have outliers like Argentina, Sri Lanka where the inflation rate is hovering around 98% and 50% respectively. At the same time you have countries like India—which is averaging 6% inflation—that have relatively been unscathed.

This trend in inflation is wreaking havoc in afflicted countries, especially given its concentration in food products. The IMF’s Fiscal Monitor put the spotlight on this and argued that this requires a strong rearguard fiscal policy response.

At one level governments need to roll back the fiscal stimulus, undertaken in the post-covid phased, to complement the efforts of central banks—who have been busy most of the last two years tightening interest rates to shrink demand.

The Fallout

Inflation in general exacts its price. But such an elevated level of inflation and so prolonged on top of it has devastating consequences.

Remember the first line of defence deployed by almost every country was to initiate lockdowns. It rendered many in the contact economy—one of the primary employers in India—jobless.

This is a double whammy therefore. At one level rising inflation erodes the purchasing power of consumers and at another, loss of jobs means being deprived of income.

This obviously impacts people differently, triggering a redistribution.The IMF believes that government intervention is key in mitigating the fallout.

Firstly, it maintains that fiscal policy cannot operate at variance with monetary policy. In the sense that while the latter is tightening monetary conditions by raising interest rates, fiscal largesse will undermine these efforts. In short, they need to act synchronously.

Secondly, the Fund makes out a case for extraordinary interventions by the government in mitigating the fallout on those at the bottom of the pyramid. Especially since a key part of this phase of inflation has been concentrated in food—which accounts for a significant proportion of household budgets.

In an interview posted on the IMF website, Paolo Mauro, Deputy Director, Fiscal Affairs Department, said (the segment in bold is my doing):

“We also suggest that whereas the overall fiscal stance should be one or fiscal tightening, it's important that the government provides support to the more vulnerable groups in the population provide some targeted transfers to the poorer segments to help them withstand this difficult time.”

The India Story

It is only natural to ask as to how India fared. As you have often read in this newsletter, India has performed relatively better.

There are several reasons for this. I will focus on two though.

First, monetary and fiscal policy have moved in tandem. Resisting temptation and consummate pressures from self-appointed advisors, the union government avoided stimulus packages raining cash during the worst of covid-19.

Even better, Finance Minister Nirmala Sitharaman actually went ahead and undertook a massive cleaning of her inherited fiscal legacy—off the book borrowings. Atoning for the fiscal sins of her predecessors actually helped win confidence on India’s budget numbers. And, after the worst of covid-19 had passed, the FM resumed the glide path to curb fiscal largesse.

At the same time, public expenditure was tweaked with unprecedented emphasis on capital expenditure—which by nature has less inflationary potential and creates a multiplier effect with respect to growth by crowding in private investments.

Simultaneously it continued to tinker with reform initiatives—some of which like slashing of corporate income tax were structural in nature and others like the farm law reforms had to be rolled back after push back from a small but well organised section of farmers.

With the benefit of hindsight, India actually adopted the IMF prescription (mentioned above) to undertake extraordinary relief measures for those at the bottom of the pyramid.

For two years it provided free foodgrains for 800 million people—by far the largest ever food programme in the world. What this did was to provide mitigation to this cohort against food price inflation.

And, remember for the last decade India has been pursuing a strategy of universalising basic material needs like electricity, housing, cooking gas, health insurance and so on. And, of course 2.2 crore covid jabs were rolled out seamlessly on a ‘One Nation, One Jab’ principle.

An improved material basis will definitely have contributed in cushioning the unprecedented economic shocks.

I have written about this in the past, but will do a quick summary of the benefits that have been rolled out so far:

11.7 crore households equipped with toilets;

9.6 crore LPG connections;

47.8 crore PM Jan Dhan bank accounts;

Insurance cover for 44.6 crore persons under PM Suraksha Bima and PM Jeevan Jyoti Yojana.

Undoubtedly, this has also contributed in lifting a record 430 million out of poverty between 2005-2021.

In the final analysis it is clear that the world, including India, is facing unprecedented challenges. The good news is that the downturn is slowing down.

The bad news is that rebuilding shattered economies will not be easy. Social turbulence could become the standard, rather than the exception.

And, all this when the world needs to stand together to combat the ill effects of climate change. Hopefully, when the going gets tough, the tough will get going.

Recommended Viewing

Sharing the latest post of Capital Calculus on StratNews Global.

This time I interviewed Shamika Ravi on the recent trend about talking up India’s potential. It started with Morgan Stanley, the global investment bank, publishing a report arguing that this was India’s Decade.

A few of us then tagged with the Digital Public Infrastructure phenomenon pioneered by India and dubbed it ‘India’s Techade’. Since then almost everyone is betting on India’s potential. Why is everyone so positive on India? And, why is everyone convinced that this time India will not flatter to disappoint.

Do listen in to the fascinating insights shared by Shamika. Sharing the link below:

Till we meet again next week, stay safe.

The current Government has figured out the formula to continue in power and is well aware that the voters in this new awakened India will allow them to govern, only if they deliver and keep improving the living standards of the entire population. In a population of 1.4 billion, where the majority are still concerned with food on their table, this Government very wisely provided free food to about 800 million people for 2 years, apart from other supportive welfare measures. This, along with an effective indigenous free vaccine program, made possible with identification through Aadhar cards, unparalleled in any other country, formed the backbone of the recovery from a once very grim situation. India always had the potential to be amongst the foremost of nations but recovering from the ravages of pre independence, a hostile neighborhood, weak leadership, corruption and lack of political will, it has taken the nation 75 years to emerge as a beacon of light for the rest of the world. A comprehensive coverage of the progress highlights Anil. Excellent piece of information and writing. Keep us updated. Thank you 😊

Dear Anil

Let me begin by appreciating the cover picture of the tulip gardens. One can now understand why Kashmir was rightly referred to as a heaven on earth. It's beauty is unmatched.

I'm surprised at the term Surprise Inflation. We are aware of the factors which have led the this worldwide inflation. What is surprising is the lack of inflation in India. How did we remain unscathed? In today's world, what affects one affects all. It's obvious that India took the right steps at the right time. Which in itself is commendable because there was no precedent as to how one can tackle something like Covid. There have been catastrophes earlier as well but nothing like Covid. Maybe it's now time for other countries to adopt The India Model.