REWRITING RISK

REWRITING RISK

2021 has emerged as the breakout year for the retail investor, suggesting that Indians are no longer inherently risk averse. EPISODE #71

Dear Reader,

A very Happy Monday to you and Eid Mubarak.

Last week I came across a stray bit of data: retail ownership of companies listed on the National Stock Exchange (NSE) had clocked a 14-year high at the end of December 2021. Interestingly, the big surge happened in the last two years following the onset of the covid-19 pandemic, which had dodgy origins in Wuhan, China.

Simultaneously we are witnessing a reset of the corporate landscape with the rapid birthing of the Unicorns in the so-called new economy. Especially since this was possible only after the Securities and Exchange Board of India, the market regulator, relaxed the rules to allow loss-making companies to list.

The Initial Public Offering of some of them—like EaseMyTrip (oversubscribed by 159 times), Nazara (175), Zomato (38) and Nykaa (81)—generated an investor frenzy, suggesting that the risk appetite of the Indian investor has grown rather dramatically. Connect the dots and what you are witnessing is an unprecedented makeover of the Indian financial markets particularly the business of risk capital.

An important subtext is that Indians are shedding their traditional risk averse behaviour. And this is a structural shift. In fact it is already finding mention in pop culture. Check out (if you haven’t already) the reality television show: Shark Tank. So this week I explore this phenomenon of changing risk behaviour of Indians.

This week’s cover picture is sourced from the Instagram feed of Akriti Sondhi, an exceptional and talented photographer. Thank you Akriti.

A big shoutout to Kapil, Aashish, Premasundaran, Yugainder, Rajit, Balesh, Ranjini, Binu, Dr Majumdar, Mr Balakrishnan, Gautam and Vandana for your informed responses, kind appreciation and amplification for last week’s column. Gratitude also to all those who responded on Twitter and Linkedin. Reader participation and amplification is key to growing this newsletter community. And, many thanks to readers who hit the like button😊.

NEW AGE INVESTORS

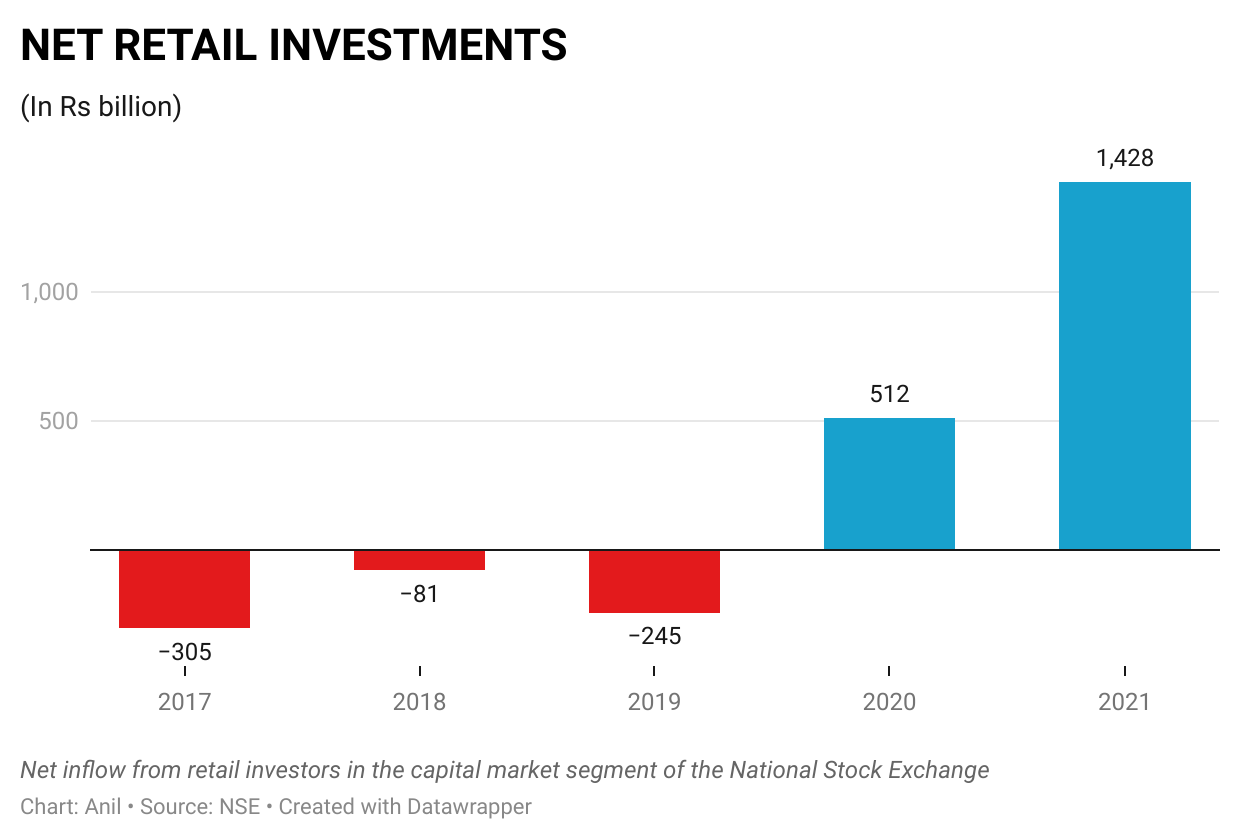

Last week the National Stock Exchange (NSE) reported that retail ownership of companies listed on the exchange had clocked a 14-year high at the end of December 2021. Interestingly, the big surge has come about in the two years after covid-19, the once in a century pandemic, struck India.

The ‘India ownership Tracker’ released every quarter by NSE estimates that in 2020-2021, inflows from retail investors aggregated Rs1.84 trillion. Of this Rs 1.43 trillion was invested last year—almost treble of the inflows in 2020.

According to the NSE, the two depositories National Securities Depositories Ltd (NSDL) and Central Securities Depositories Ltd (CDSL), registered 14.3 million investors in 2020-21. In the first 11 months of 2021-22 the addition of new investors more than doubled to 31.8 million.

Further, the share of individual investors in the cash market (where the sale and purchase of equity is settled at the point of sale) was 45% in 2020-21 and 41% in the first 11 months of 2021-22.

Clearly, 2021 has emerged as the breakout year for the Indian retail investor.

The Wang Trifecta

Wrapping one’s head around this trend can be difficult. How does a traditionally risk averse country embrace the stock markets with such abandon.

Like every trend, this development has not happened overnight. It is the outcome of a happy convergence of circumstances that is enabling unprecedented empowerment of the cohort of Indians who have disposable income and are desperate to better their lifestyle and save for the future.

I have written about this convergence previously, but believe that it is best summed up by the moniker Sajith Pai so famously coined: The Wang Trifecta.

Some years ago Pai met up with Tony Wang, cofounder of @agoraIO and asked him to unpack China’s success story with respect to consumption. Wang responded by saying this was enabled by the coming together of three trends:

Cheap bandwidth;

Smartphone in every pocket;

A frictionless payment system.

Unlike in China, the Wang Trifecta is still a work in progress in India. Yes some demographic segments have already realised these standards, but bulk of the Indian population continues to be outside this framework.

However, there is a marked difference in the post-Jio era—the cost of 1 GB of data dropped from Rs 250 to less than Rs 10; exactly why almost everyone around is consuming viral content.

In terms of frictionless payments, the Unified Payments Interface (UPI) has emerged as a world class product. It is, as pointed out previously, transforming the payments business. From a few thousand transactions that it averaged after its launch in 2016, UPI has scaled dramatically since. In March this year it had registered a staggering 5 billion transactions.

Smartphone usage has no doubt witnessed a dramatic growth from about 15 million in 2011 to little under 200 million in 2021. Yet, it is clear that bulk of the population is still using feature phones.

So the network effect of the Wang Trifecta is yet to be realised to its full potential. It is working for sections of the population. And where it is visible, like in the instance of retail investors, the impact is quite dramatic.

The Breakout Year

The data shared above clearly establishes 2021 as the tipping point in the history of retail investors in India. The transformation is not just in the number of the new investors it is also about their attitude towards risk—in its assessment and management.

A survey—'How New-age India Invests: Changing mindsets, goals and risk-understanding'—conducted by NielsenIQ for the NSE seeks to decode this makeover of the retail investor.

The reasons driving this were identified as:

Financial security in case of emergencies (44%)

Retirement planning (43%)

Financial security for family members (42%)

Mental and physical well being (41%)

And their risk appetite is spread over:

Equities (45%)

Cash market/IPOs/NCBs (39%)

Derivatives (32%)

Government securities/debentures/bonds (26%)

I was struck by the reasons inspiring the new approach to risk, particularly with the desire to underwrite unexpected developments and retirement. Underlying this maturing of the retail investor is the growing longevity of Indians and their material trading up.

The survey found that the preference for derivatives, a segment with greater risk, is among the younger cohort of investors—less than 45 years of age and earning more than Rs50,000 per month. Yet a third of them also preferred the safer route of mutual funds.

Indeed the big takeaway is that the Indian retail investor has changed. And that this transformation is irreversible. In turn the new risk appetite is also enabling the emergence of start-ups—many of whom are yet to turn in profits. Together with all the other changes I chronicle every week it is apparent that India is transforming, albeit slowly.

Recommended Viewing

Last week the Vidhi Centre for Legal Policy hosted a webinar to discuss the latest book by Gyan Prakash, Dayton-Stockton Professor of History, Princeton University, which revisits the imposition of the Emergency on 25 June 1975.

The book, ‘Emergency Chronicles: Indira Gandhi and Democracy’s Turning Point’, examines this aberration by going back to the framing of the Constitution of India and how our Founding Fathers made a conscious choice in empowering the government with such extraordinary powers. I found the why of this decision fascinating.

If you can’t read the book, do take time to view the webinar link I have shared above.

Till we meet again next week. Stay safe.

Very nice article uncle!! And a true reflection of a trend which I can honestly see in my own finances. A key factor has just been awareness and discussions. In the past, if you found a good investment opportunity, the advice was to keep it to yourself or maybe just to close ones. Now we have access to a plethora of sites which provide information and a number of content creators on Instagram and FB who make videos on investments. This combined with the drop in interest rates on SB and FDs as well as lower returns on real estate meant that today there are very few options outside the stock market to beat inflation. The tax regime also aided the same as till recently dividends were tax free. Hopefully going forward personal finance management and education become a part of curriculum in higher secondary schools as well as colleges.

Dear Anil,

Well researched and interesting article, you are absolutely correct in saying that Indian investors is changing!! Risk taking and more diversified portfolio is the new norm.The LIC ipo is grabbing headlines everywhere, and in discussions.

Beautiful picture by talented Akriti is a treat for the eyes !!