REVISITING THE UNION BUDGET

REVISITING THE UNION BUDGET

The economic shock triggered by the crisis in Ukraine merit a review of the inbuilt safeguards in the Union Budget for 2022-23. EPISODE #62

Dear Reader,

A very Happy Monday to you.

Last week, unmindful of the warnings from the Western Block led by the United States, Russia carried out the threat it has bandied around for the last year and more by invading Ukraine. Besides being a fresh reaffirmation of the gradual end to US hegemony and an imminent reset of the global high table, it has triggered an economic shock.

The usual barometers of economic health, stocks and commodities, have gone into a tizzy. Given the recent disastrous history of similar invasions—Afghanistan and Iraq—by a super power, no one has a clue when the dust would settle. More worryingly it is not clear as to how this confrontation would end.

The economic shockwaves will spare no country, including India. The spike in crude prices to a seven-year high is a signal that uncertainty around Ukraine could roil the macroeconomic environment. And this when the global economy is just about limping back to normalcy.

It may be worthwhile then to reexamine the shock absorbers built into the Union Budget for 2022-23. Whether they are sufficient to deal with this unexpected challenge.

Though the Budget has been presented to Parliament, it is yet to be passed. Indeed if a review does reflect the need to rework the assumptions, then this would be the best time to do a reset. And coincidentally this week’s episode arrives in your mailbox on the last day of February—the traditional date for Budget.

I owe this week’s subject idea to Haseeb Drabu, a gifted thinker, economist, friend and co-author. Read on and do share your feedback. This week’s cover picture is an installation art I discovered abandoned in a corner of Kochi airport.

A big shoutout to Gautam, Vandana, and Ajay for your informed responses, kind appreciation and amplification for last week’s column. Gratitude also to all those who responded on Twitter and Linkedin. Reader participation and amplification is key to growing this newsletter community. And, many thanks to readers who hit the like button😊.

RUSSIA GOES TO WAR

I guess it is for a reason that Shakespeare famously warned about the ‘Ides of March’ in Julius Caesar. One is overcome by a feeling of deja vu as another daunting March looms ahead.

Exactly two years ago the world was waking up to the threat of the covid-19 pandemic, which had dodgy origins in Wuhan, China. What followed was a once in a century health shock, which rapidly morphed into a global economic meltdown as countries went into lock down. You may recall the Indian economy contracted by a record 23.9 % in the first quarter ended June of 2020-21.

Just about when the world was beginning to see the back of covid-19, which has shown remarkable resilience by assuming various lethal avatars, the Russians launched an invasion of Ukraine last week. Talk of coincidences! Now the big worry is whether the world economy will slip back into the hole.

The Indian economy too is vulnerable. The good news though is that it displayed remarkable resilience and rebounded. This quarter it erased the deficit.

However if the conflict is prolonged and other countries are drawn into it, the economic risks will multiply and could derail the nascent recovery that is underway.

The Threat

There is no doubt that the biggest threat is that of imported inflation. The fact that Russia is an important part of the oil economy, make oil prices particularly susceptible. Luckily oil sanctions are off the table and oil prices have dropped from the $100-plus high it had touched immediately after the conflict began.

But oil is only part of the problem. Other commodity prices too have increased, actually much before the conflict. It is part of the trend of hardening inflation trends worldwide—largely caused by a disruption in supply chains in the aftermath of the covid-19 pandemic.

The good news is that Nirmala Sitharaman’s fourth budget has some in-built shock absorbers.

Firstly, relative to what analysts anticipated she has been conservative in her growth projections for 2022-23. The FM assumed a nominal growth rate of 11.3% in 2022-23, while analysts were expecting around 13%.

In her first post-budget interview granted to Doordarshan I had specifically queried her on the logic of this decision.

Wiser after being blindsided by the ferocious fallout of the Delta wave of covid-19, Sitharaman explained that her budget anticipated some economic shocks, especially of rising commodity prices, and therefore preferred to err on the side of caution.

Yes, the Ukraine episode was unexpected, but clearly the Finance Ministry cannot be accused of not having a plan. It is another matter whether it will prove sufficient to absorb the emerging economic shocks.

“Now Omicron (wave) is on, but even more (importantly) you have the US Fed (raising interest rates), the international crude oil prices (are) going up, metals have become very expensive.

So we will have to keep all this in mind. We are not getting into details of which is considered a challenge, which is a headwind and which is not.”

Secondly, the expenditure estimates for 2022-23 are pegged reasonably close to the massive outgo the union government had to undertake in the aftermath of the pandemic. The point is that this was an abnormal spike caused by an unprecedented crisis and pegging spending at this level is therefore prudent.

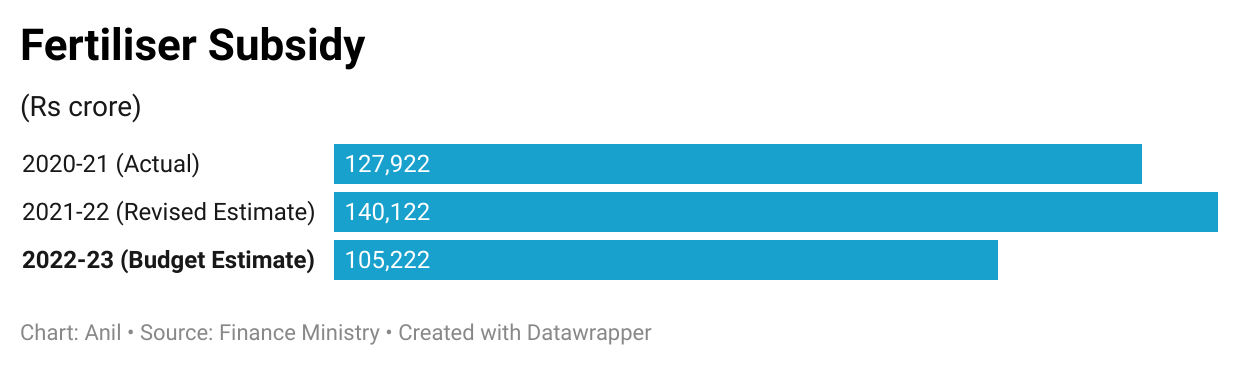

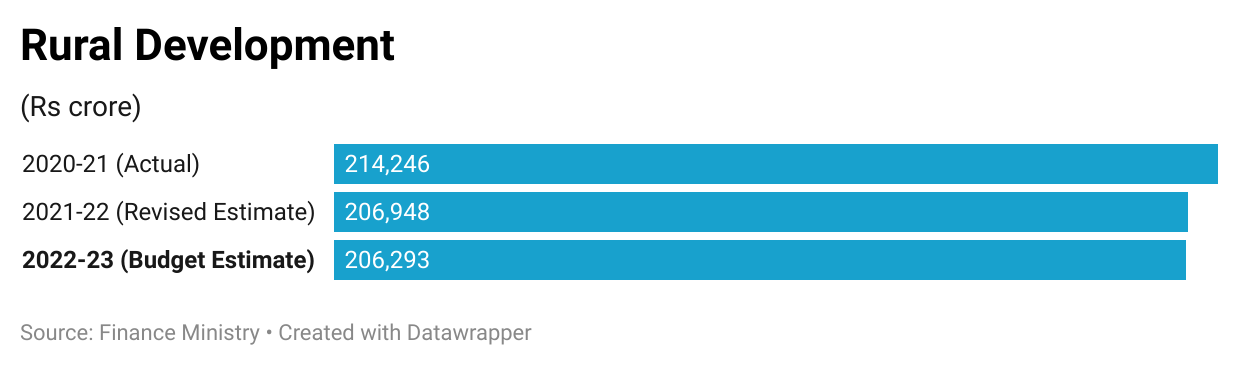

I am fleshing out two sub-heads of big ticket spending on welfare programmes to mitigate the fallout: Subsidies and Rural Development.

In the case of food subsidy the abnormal surge in actual spending in 2020-21 was high because the government cleaned its books by bringing the off-the-book subsidies—the collective sins of previous regimes—buried in the balance sheet of the Food Corporation of India.

Excluding this the rest of the increase in food subsidy is explained by the government’s decision to provide free food grains to 800 million people for the last 18 months. The projections in 2022-23 seem lower because the free food grain scheme is scheduled to come to an end on 31 March. Yes, if it is extended the Union Budget will have to absorb the increased spending.

Part of the increase in fertiliser subsidy was caused by a big spike in international prices last year. The expectation is that these prices have peaked—however the Ukraine fall out could upset this math.

In the instance of rural development, the data clearly shows that the FM is following recent trends. An additional point is that the Mahatma Gandhi Rural Employment Guarantee (MGNREGA) scheme, the social safety net guaranteeing employment, is demand-based and hence the amount paid out fluctuates.

If rural distress worsens then MGNREGA budget will have to be hiked as it is mandatory for the union government to service this demand.

In fact, FM Sitharaman said as much in the same Doordarshan interview in response to my question.

“When programs are demand driven we fund it as and when we get the data. So if at the moment you see that this amount will take care of the immediate couple of months we give it and there is always a supplementary demand in the Monsoon session and in the winter session (of Parliament) through which we can always bring in additional resources which is required many of these programs.

Because they are demand driven you really cannot estimate what will happen after three months and so there is no point in putting it up front.”

Finally, the revenue projections for 2022-23 seem to be modest. Against a record surge of 16.2% to Rs20.78 lakh crore in 2020-21, next year’s budget projects growth at 6.1% to Rs22.04 lakh crore.

More importantly the Budget has not accounted for the likely recovery of the contact economy—which otherwise has been battered beyond recognition in the last two years. With the national jab project drawing to a close with the target group close to receiving their two jabs and the covid-19 pandemic slowing in its spread as well as intensity there is every reason to believe in the revival of the contact economy; this is likely to cause a commensurate impact on revenues accruing to the exchequer.

If this does pan out then FM Sitharaman has a pleasant upside to growth inbuilt in next year’s Budget.

In the final analysis it is clear that there are some shock absorbers built into next year’s Union Budget. The obvious question is whether they are sufficient. Especially since no one has a clue as to how the Ukraine imbroglio will play out.

If the conflict concludes quickly then the world economy can get back to mending itself. If not all bets are off. As they say no plan survives the first contact with the economy. To be fair it is simply impossible to ready a safety net to deal with two back-to-back shocks posed by the once in a century covid-19 pandemic and the Ukraine conflict.

But if it is of any comfort, the experience of the last two years is cause for optimism. The government demonstrated its ability to think out of the box and unleashed a series of mini-budgets to stimulate the economy and protect livelihoods. But this was ex post. The review I am proposing is an ex ante approach.

The ball is in the FM’s court.

Recommended Listening

Last week the trio of Debu Mishra, Srinath Sridharan and me restarted our NooTopic conversations on Twitter Spaces.

This time we explored the Future of Writing in a digital era—which has disrupted the conventional business of writing.

The panel included two first-time authors—Surabhi Prasad and S Venkatesh—and an audio-book publisher—Ratna Saksena—and threw up some great insights and terrific tips for first time writers. Salute also to some very accomplished listeners who joined the conversation midway; typical of the serendipity associated with the discovery process of social audio platforms like Twitter Spaces and Clubhouse.

Sharing a quote by Venkatesh as a teaser.

“I think the interesting thing we are seeing is that across the board the definition of writing, storytelling is changing. It is no longer just about writing a book.

The same person could be writing a book; writing part of the screenplay for a web series; writing a column on Substack or sharing threads on Twitter.

So there is a lot of opportunity. But at the same time the space is also very crowded. To stand out is therefore that much more difficult today than it was 20 years ago.”

I would recommend you listen to the entire conversation by clicking this link. (Please keep in mind that this link expires in a month.)

Till we meet again next week. Stay safe.

During the interview with FM Shrimati Nirmala Sitharaman ji, you had asked her Anil, whether there will be a periodic review of the budget and she had promptly answered in the affirmative; informing that it will be the way to proceed and every 3 months or so, the progress will be reviewed and whatever changes that are required, will be introduced. At the time of the interview, the unknown factor was the pandemic and it cannot be entirely ruled out; but today the new reality is the war in Europe and the involvement of many countries throughout the world. With Brent crude oil prices at over $103 a barrel today , hardening of prices in metals and some other commodities, it looks like a tough road ahead for the world and Indian economy specifically. However, with the pent up demand being released, many sectors, especially travel and tourism and the manufacturing and services sectors are set to take off. If agriculture continues the good performance of the past few years, then the growth by the third quarter could be around 15%. With employment picking up, India's festival and especially marriage season should be able to peak the demand for goods and services, leading to a robust economic development. Inflationary pressures will be there, coupled with an uncertain world peace. The relevant points have been very well encapsuled. Thanks for sharing this.

Dear Anil,

You have analyzed the impact of Russian and Ukraine conflict so well.It has already rattled the global stock markets and sparked anxiety around personal Finances across the world which have already been strained due to the pandemic. The far reaching and destabilizing economic impact of this conflict could jeopardize the world s financial recovery.

Ukraine is called the bread basket of Europe and food supply chain may also be hit hard .India imports oil from Russia and sunflower oil from Ukraine. Due in increase in oil prices which have reached more than 100 $ a barrel, inflationary pressures willl slow down our economic growth.

We need to rethink some of our policies and hope for an early end of the conflict !!