INDIA SHINING

The World Bank's annual update echoes the visible pivot in the world's perception about India in general and its economy in particular. EPISODE #103

Dear Reader,

A very Happy Monday to you.

Last week the World Bank published its India Development Update (IDU), capturing the latest outlook for the Indian economy. Not only does the Bank believe that India has done well in the exceptional circumstances overwhelming the world, it believes the country’s best is yet to come.

In many ways it echoes the optimistic projection by Morgan Stanley arguing that this was India’s decade for the taking.

So this week I put the spotlight on this very visible pivot in the perception about India in general its economy in particular. Do read and share your feedback.

Coincidentally, last week’s episode of Capital Calculus on StratNews Global focuses on what I call ‘India’s Techade’. Anjali Bansal, founding partner of Avaana Capital, lays out very clearly as to why indeed this is India’s moment to seize.

The cover pix is a panoramic view of another vertical city.

A big shoutout to Niranjan, Ranjini, Aashish, Gautam, Premasundaran, Vandana and Prasanth for your informed responses, kind appreciation and amplification of last week’s column. Gratitude also to all those who responded on Twitter and Linkedin. Reader participation and amplification is key to growing this newsletter community. And, many thanks to readers who hit the like button😊.

Happy to report that last week’s episode—India’s Moment—has resonated really well with the growing tribe of readers. Thank you reader.😊

THE OUTLOOK

Last week the World Bank put out its update on the Indian economy.

The mid-year review did the unthinkable: it upgraded India’s growth projections for this year, one in which most of the world economy is in shambles. It was also an ode to India’s ability to negotiate the covid-19 storm.

And, the Bank did not stop here.

It went on to argue that thanks to the growing prowess of its digital economy, India is emerging as the lighthouse for the world. Taking up from where Morgan Stanley left off arguing that this was India’s decade for the taking, the Bank maintains that the country’s best is yet to come.

Beyond the optimistic projections about India’s prospects, there is another important sub-text: A clear pivot in the way the rest of the world views India.

And the litmus test for this rethink on India is the grudging admiration being expressed by Western media—who normally operate with visible bias when it comes to reporting about the country. (This is actually surprising given that most of these journalists are exceptionally talented and some of them have taught me so many reporting and analytical skills.)

The Rethink

In April last year the Economist, inspired by the relentless doomscrolling no doubt, did this cover story on India. It essentially wrote off the country as one which had failed to read and deal with the covid-19 pandemic, which had dodgy origins in Wuhan, China. The reality of course was that India was severely bruised, like every other country, but it managed to survive—despite its sell-past-the-date health infrastructure.

And little over a year later the same magazine did a stunning flip-flop.

Of course they could not resist condescension and stuck a line in their cover: “Will Modi blow it?”

My point here is not about the misreading—which could either be an error of omission or commission—of India’s changed circumstances by mainstream global media and their Indian cohorts. There is enough evidence out there, which a discerning reader like you would have observed.

Instead it is about this pivot in the global perception about India. What changed in the last one year?

As a regular reader of this column you would be aware that I have dwelled regularly on the fundamental transformation that has been underway for over a decade now. Especially the role played by technology in using digital public goods (DPG) to empower at scale. We are talking about a new paradigm of growth—this is not visible if viewed with the traditional prism.

To cite one example, 12 years ago 430 million people did not have a bank account. And now, thanks to Aadhaar, they do. Even better, thanks to the Open Credit Enablement Network—and other DPG like Aadhaar—they are queuing up for sachet credit of sums as low as Rs150! The digital backbone has enabled the lender to afford the cost of servicing loans in such small sums.

In short, the rest of the world has come late to the party.

The Report Card

The World Bank’s rosy annual update has come at a very interesting moment.

The union finance ministry is readying to present the next Union Budget—and also the last in this tenure of the Bharatiya Janata Party (BJP)-led National Democratic Alliance (NDA)—before the next general election in 2024. The validation from an external agency, and that too a multilateral body, would be welcome.

Implicitly it is an endorsement of the playbook North Block had adopted in mitigating the devastating fallout of the covid-19 pandemic, threading together a recovery—entailing a government-led step-up in capital expenditure—and then holding the economy together as it battled through fresh economic shocks.

Never before has the world suffered three back-to-back shocks of this economic magnitude. Barely had the impact of the covid-19 pandemic started to peak, the Russia-Ukraine conflict roiled global supply chains afresh—causing a massive surge in inflation world-wide.

To battle it the United States Federal Reserve unleashed a massive round of interest rate increases.

Not only did this dry up global liquidity it also pushed up the value of the dollar, inducing a devaluation of most global currencies (including the Indian rupee)—which essentially meant that the US is exporting inflation as countries with devaluing currencies are seeing a rise in the cost of their imports.

In these circumstances the performance of the Indian economy is not only impressive, but it has surprised most critics.

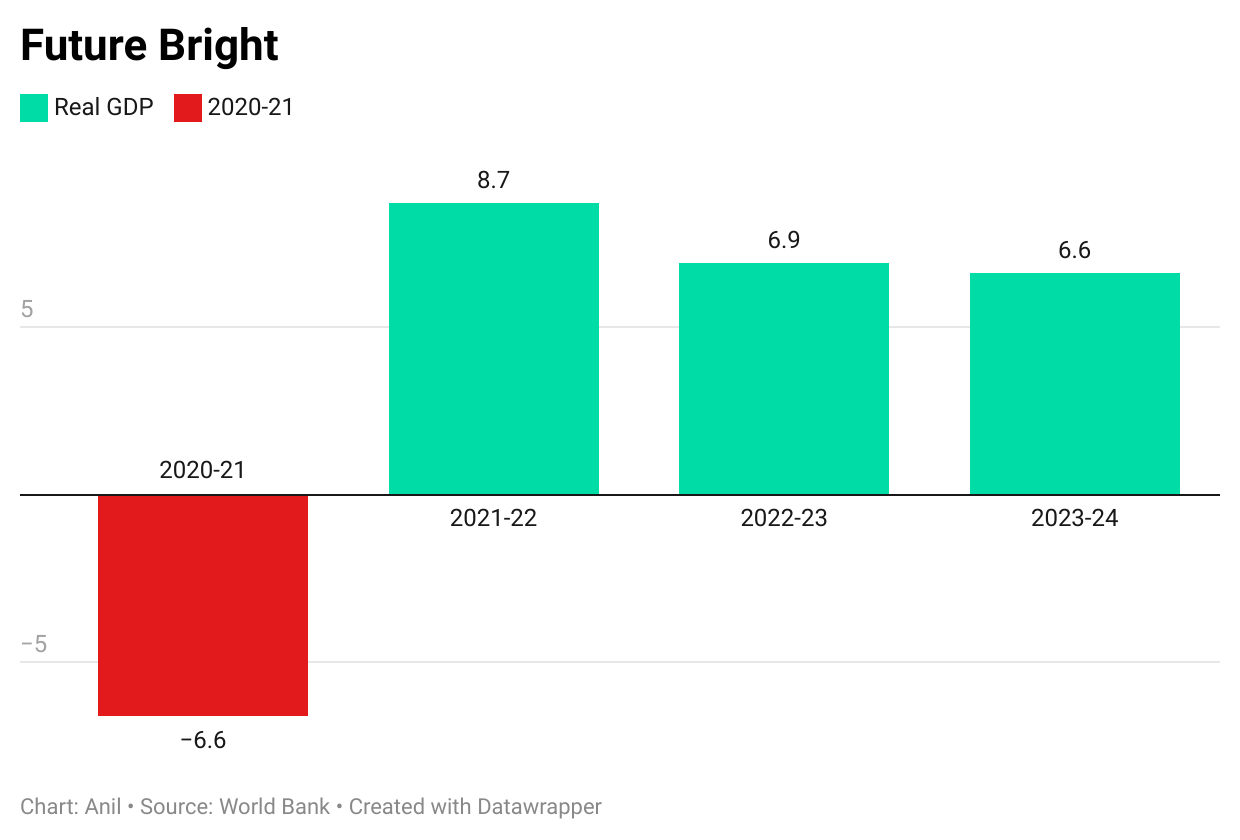

As the graphic above—carried in the World Bank update—shows the Indian economy contracted during the covid-19 wave and then rebounded. It is remarkable that the Indian economy is projected to grow at 6.6% in 2023-24—a year in which most of the world may well be sinking into recession.

And the World Bank says as much:

“India faced a challenging external environment following the Russia-Ukraine war with elevated crude oil and commodity prices, persistent global supply disruptions (caused by the global shortage of shipping containers and supply bottlenecks) and tighter financing conditions. This created domestic inflationary pressures.

Notwithstanding these challenges, real GDP grew by 6.3 percent year-on-year (y-o-y) in Q2 FY22/23 (July- September), driven by strong private consumption and investment.

The government’s focus on bolstering capital expenditure also supported domestic demand in the first half of FY 22/23. In addition, India overtook the UK to become the fifth largest economy in the world.

High frequency indicators indicate continued robust growth of domestic demand at the start of Q3 FY22/23.”

And then added:

“India’s economy is relatively more insulated from global spillovers than other emerging markets. India is less exposed to international trade flows and relies on its large domestic market. India’s external position has also improved considerably over the last decade.”

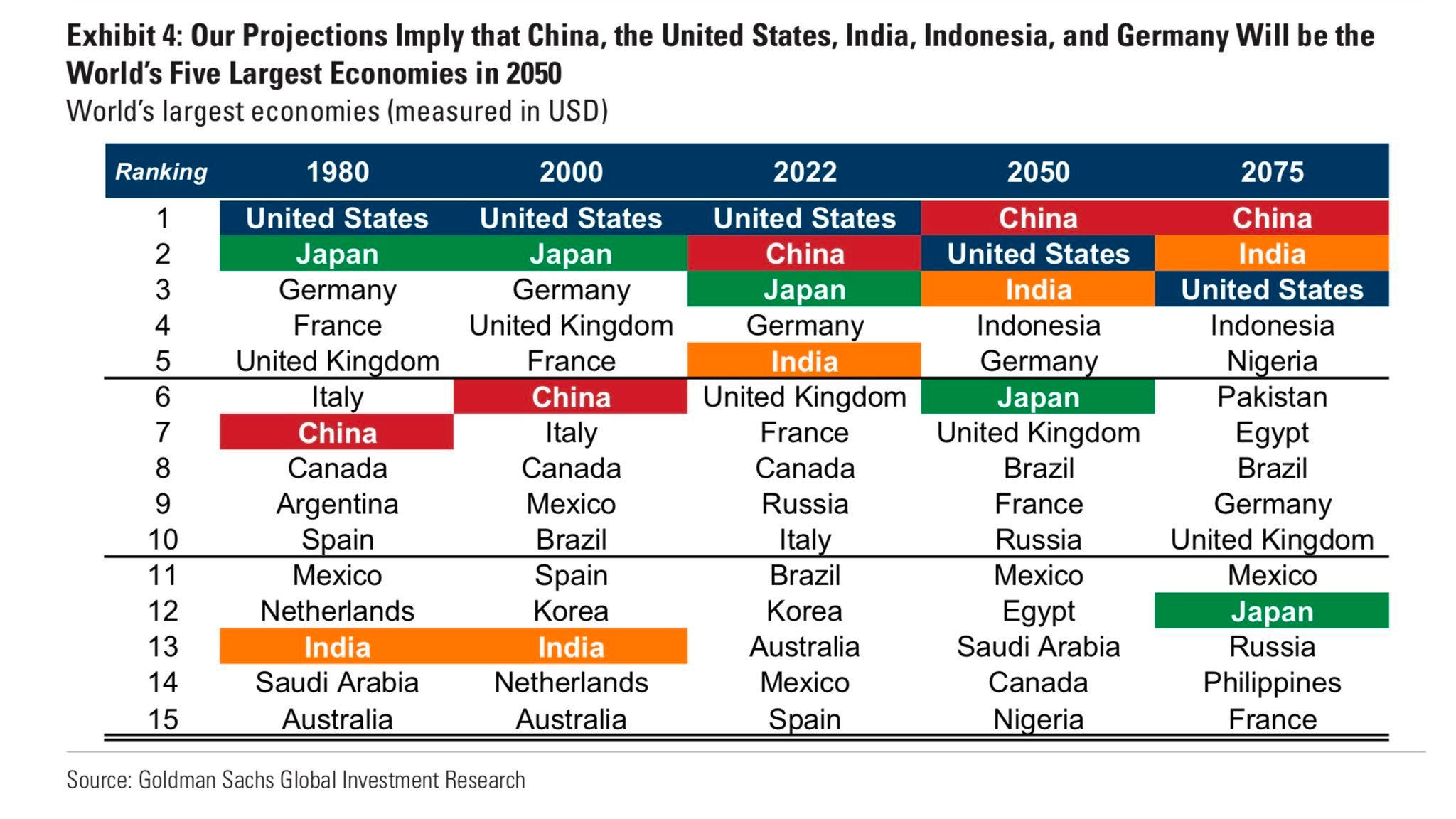

This is not an instance of one swallow makes a summer. Morgan Stanley, World Bank and now Goldman Sachs are arguing the same.

Its forecast of the largest economies in the next 50 years claims an end to the era of exceptionalism of the United States and lists India as the second largest economy in the world.

More importantly it shows that the world will be realigned. The biggest loser will be the Western world, who for long have punched way above their weight. If the forecast holds good it shows that Asia will be the new center of the world by 2075. Yet the world will be far more balanced with representation from the African continent. Presumably this also means a more peaceful world.

This graphic makes clear as to why India is beginning to be perceived as a lighthouse of the world economy. Its leadership of the G20 grouping of nations has come at an opportune moment. The big challenge for India now is to measure up to this burden of expectations.

Recommended Viewing

Sharing my latest post on StratNews Global.

As I explained in the introduction, this segues very well with the newsletter episode this week. The guest, Anjali Bansal, dwelled on the range of issues which are inspiring the confidence of the rest of the world in India. Do watch and share your thoughts.

I am sharing the link below:

Till we meet again next week, stay safe.

Our stars seem to have aligned. While there is promise, much will depend upon how we execute as Team India. While Sensex is at record high and cities are shining, I do hope things are strong on the ground too. Biggest opportunity is our young population; hope we can create enough jobs for them. Let's hope and pray we can do it. Jai Hind.

Dear Anil

I have to admit that your articles do make one more and more proud of India's achievements. Every week can aptly be titled India's Moment. The upgrading of India's growth projections for this year by the World Bank as well as the validation of India's position vis-a-vis the world is most heartening. That too when most of the world economies are in shambles. Such a scenario would have been unimaginable a few years back and it's a reflection of the way things will be in the future. Whether the other countries love us or hate us, they can no longer ignore us.