GLOBALISING UPI

The digital handshake between India and Singapore enabling cross-border, real time payments is one more step in globalising UPI. EPISODE #115

Dear Reader,

A very Happy Monday to you

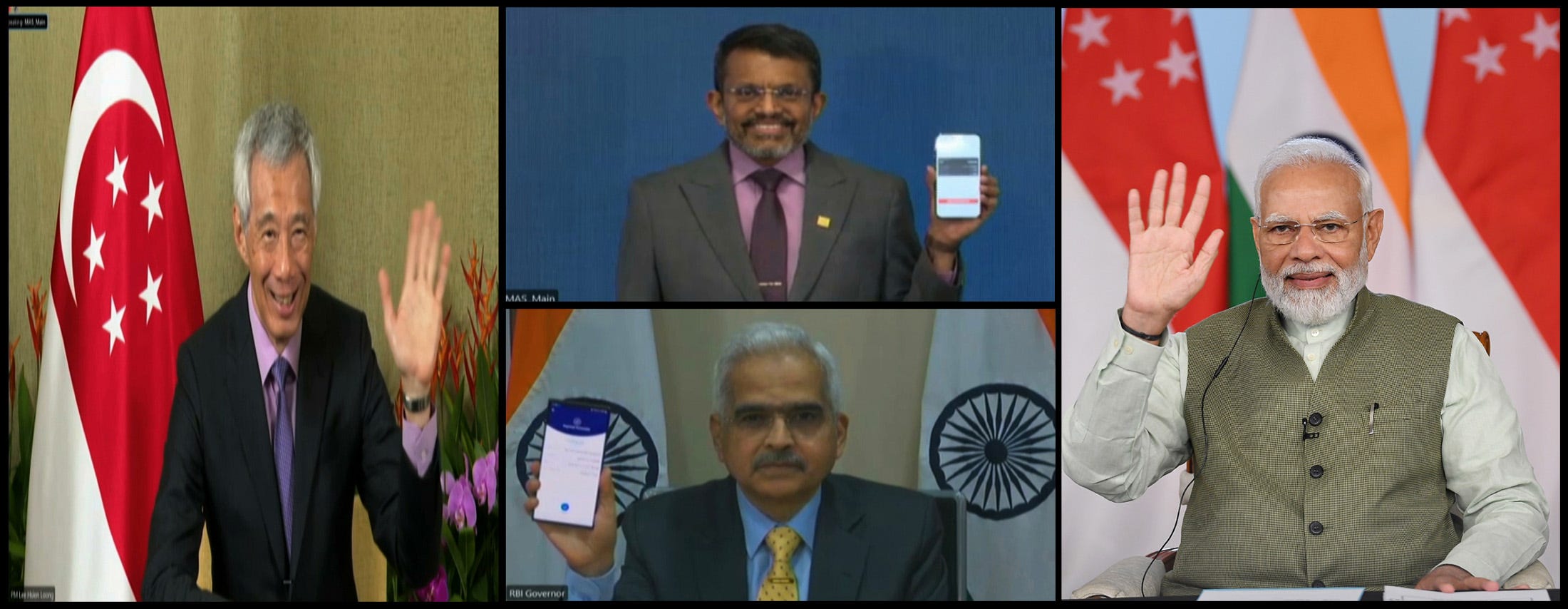

Little under a fortnight ago India and Singapore enabled a real time payment linkage, wherein residents of both countries could undertake cross-border transactions using their mobile phones.

Overnight, the international footprint of the Unified Payments Interface (UPI), the real time payment mechanism from the stable of the National Payments Corporation of India (NPCI), acquired a stronger international footing.

Essentially UPI is poised for a new growth phase. This week I examine UPI 2.0 and the attendant implications.

The cover picture this week is a screen grab from the event launching the new payments bridge between the two countries.

A big shoutout to Shiv, Gautam, Vandana, Aashish, VK, Debu, Premasundaran, Balesh, Balasurya and Laxmi for your informed responses, kind appreciation and amplification of last week’s column. Once again, grateful for the conversation initiated by readers. Gratitude also to all those who responded on Twitter and Linkedin. Reader participation and amplification is key to growing this newsletter community. And, many thanks to readers who hit the like button😊

UPI 2.0

Little under a fortnight ago, India and Singapore inked a deal enabling real time cross-border transactions between the two countries.

Accordingly, the payment bridges of both countries, Unified Payments Interface (UPI) and PayNow have been linked. While UPI is offered by the National Payments Corporation of India (NPCI), PayNow is the equivalent in Singapore.

PayNow, like UPI, provides a peer-to-peer funds transfer service to the retail customers of 10 participating banks and four participating Non-Bank Financial Institutions (NFIs) in Singapore—Bank of China, CIMB Bank Berhad, Citibank Singapore Limited, DBS Bank/POSB, HSBC, Industrial and Commercial Bank of China Limited, Maybank, OCBC Bank, Standard Chartered Bank, UOB, GrabPay, LiquidPay, Singtel Dash and Xfers.

The infographic above, sourced from PayNow, explains the money transfer process. An estimated $1 billion in annual transactions between the two countries will now happen in real time and at substantially lower cost.

As an aside, India accelerated its bid to disrupt the global payments business, just like UPI did within the country.

The thing is that while this was a country-to-country deal, a subsidiary of NPCI, NPCI International Payments Limited, has been stitching together deals with banks in various countries to globalise RuPay and UPI. Earlier, NPCI International had signed a deal with Mashreq Bank in the United Arab Emirates to enable UPI transactions.

The initial idea was to develop a “huge acceptance network” for both these instruments to enable seamless payment for Indian travellers to these countries. Now, the scale of this effort is transformative.

This ease of living aspect of UPI was best captured by Radhika Gupta, Managing Director and Chief Executive Officer, Edelweiss Asset Management Limited, when she said on Twitter:

“It is when you travel abroad that you realise how much UPI has spoiled us in India.”

Sharing the tweet below, in case you wish to read the conversation thread.

The UPI Foundation

As a regular reader of this newsletter, you would know that I frequently dwell on India’s unique digital economy. With the launch of Aadhaar, the unique 12-digit identity, in 2009, India has progressively built out the most extensive Digital Public Infrastructure (DPI) in the world.

Its uniqueness—now being embraced globally—lies in the fact that this DPI is open and allows anyone, government or private sector, to build innovations on these digital rails.

One of these innovations includes UPI, which completely revolutionised payments in the country. After a quiet start, use of UPI has grown exponentially. As the graphic above shows the volume of transactions is almost doubling every year.

In January this year, transactions using the UPI topped 8 billion—in February it fell below this record. Of this nearly two out of three transactions were for sums less than Rs500—the bottom of the pyramid is an enthusiastic player and are gradually joining the formal economy.

While UPI has hogged the headlines, NPCI is much bigger. It has combined with Aadhaar, the 12-digit unique identity, to create a world class payments bridge—which can be used for a range of functions, including UPI.

You may not know that NPCI enabled the Direct Benefits Transfer (DBT) on welfare payments by the Union Government. It did so by forging an economic GPS by combining the mobile number of a beneficiary with their Aadhaar and bank account. Cumulatively this has saved Rs 3 lakh crore to the national exchequer in leakages, while ensuring the payment reaches the intended beneficiary in real time.

Sharing below the entire bouquet of services provided by NPCI.

RuPay: An indigenously developed payment system that supports the issuance of debit, credit and prepaid cards.

IMPS: Immediate Payment Service (IMPS) enables real time payments in the retail sector.

NACH: National Automated Clearing House (NACH), an offline web-based system for bulk push and pull transactions.

APBS: Aadhaar Payment Bridge (APB) system enables DBT for various Central as well as State sponsored schemes.

AePS: Aadhaar enabled Payment System (AePS) enables door-step delivery of funds, thus providing a big fillip to financial inclusion.

NFS: National Financial Switch (NFS) is the largest network of shared Automated Teller Machines (ATMs) in India.

Bharat Bill Payment System: Offers one-stop bill payment solution for all recurring payments with 200+ Billers for utilities like electricity, gas, water, telecom, DTH, loan repayments, insurance and so on.

NETC: National Electronic Toll Collection (NETC) enables electronic tolling or the ubiquitous FastTag

Presumably, like me, you too are impressed as to how, in just six years, an Indian innovation has won the acceptance of the world. The agreement with Singapore is only the beginning.

As I always say, India’s cup is half-full and not half-empty.

Recommended Viewing

Sharing the latest post of Capital Calculus on StratNews Global.

This time I put the spotlight on the Union Budget that was presented by Finance Minister Nirmala Sitharaman. Revisiting the FM’s speech I observed that the FM made 24 specific references to the word “green”. It only confirmed the significant pivot India is undertaking to make it carbon neutral by 2070.

I was curious as to how this would play out at the ground level and spoke to Sameer Aggarwal, CEO of RevFin. RevFin finances the purchase of Electric Vehicles in Tier-2, Tier-3 cities—essentially serving those at the bottom of the pyramid.

In a very insightful interview he laid out the alacrity with which three-wheeler EVs are being embraced and deployed in Tier-2, 3 cities and how they are enabling an unprecedented socio-economic transformation.

Do watch and share your thoughts. I am sharing the link below:

I am also sharing my latest column published in the Economic Times.

It picks up from my post-budget thoughts shared in a previous newsletter. Do read and share your feedback.

Till we meet again next week, stay safe.

Dear Anil,

Enjoyed reading your informative and unbiased article. Digital India is progressing by leaps and bounds.It is playing a key role in modernization of trade and buisness, and also in integration of our rural economy.The Economic Times article also is very good and give an overall perspective.

Dear Anil

Really enjoyed the well researched article on the globalising of UPI. Let me start by referring to Radhika's comment. I don't travel abroad frequently but frankly I can't now imagine traveling within the country without the ever so convenient UPI. It has truly spoiled us. Gone are the days when it was mandatory to regularly withdraw cash for meeting household expenditures- not to mention travelling. It's such a proud moment for our country that we can actually undertake even cross-border transactions. To think that the very idea of UPI was scoffed at by a few learned people till a few years back. Six years is such a short time in order to not only become indispensable within the country but also gain global acceptance. No doubt that like you, I'm genuinely Impressed.