DOLLAR DETOX

The debate over de-dollarisation is gaining decibels, but is such a circumstance even conceivable? EPISODE #124

Dear Reader,

A very Happy Monday to you.

Last week Uday Kotak, the founder and outgoing CEO of Kotak Mahindra Bank, set the cat among the pigeons by calling out the United States dollar, the world’s reserve currency, as a “financial terrorist”.

Though, he tried to walk back his sharp remarks the next day by taking to Twitter, the veteran banker had succeeded in dialling up the debate over de-dollarisation.

This week I explore the idea of de-dollarisation and try to answer some tough questions: Is it even conceivable, given that 80% of global currency transactions are dollar denominated? What will be the alternate reserve currency? And what will be the cost of making this transition?

The cover photo is a provocative picture taken by JP Valery and sourced from Unsplash.

A big shoutout to Balesh, Joy, Yugainder, Sangeeta, Vandana, Ranjini, Gautam and Premasundaran, for your informed responses, kind appreciation and amplification of last week’s column. Once again, grateful for the conversation initiated by all you readers. Gratitude also to all those who responded on Twitter and Linkedin. Reader participation and amplification is key to growing this newsletter community. And, many thanks to readers who hit the like button😊.

DEDOLLARISATION

Addressing the Economic Times awards ceremony for corporate excellence last week, Uday Kotak, founder and outgoing CEO of Kotak Mahindra Bank, made a sensational claim by arguing that the US dollar, the reserve currency of the world, was the “biggest financial terrorist”.

“The biggest financial terrorist in the world is the US dollar.

All our monies are in Nostro accounts (a foreign bank holding US dollars in an American bank) and somebody in the US can say that you cannot withdraw it from tomorrow morning.

And, you are stuck. That is the power of the reserve currency.”

To be sure, Kotak is not the first to voice such concerns. And, will certainly not be the last.

Last month, President Luiz Lula of Brazil launched a similar broadside against the US dollar. And, he made this statement during an official visit to China—a country which has sought to challenge the dollar’s as well as US hegemony.

“Every night I ask myself why all countries have to base their trade on the dollar. Why can't we do trade based on our own currencies.

…Who decided that our currencies were weak, that they didn't have value in other countries?

…Why can't a bank like that of the BRICS (Brazil, Russia, India, China, South Africa) have a currency to finance trade relations between Brazil and China, between Brazil and other countries?

It's difficult because we are unaccustomed. Everyone depends on just one currency.”

And, then over the weekend, a precocious 13-year old American asked Warren Buffet as to why de-dollarisation is gaining momentum. And, what was his company doing about this? Check out the video below:

Buffet’s response was interesting.

“Nobody knows how far you can go with a paper currency before it gets out of control, particularly if you are the world's reserve currency.”

To be fair to Kotak, he tried to walk back his sensational remarks the next day, through a post on Twitter.

Regardless, the queries posed by both Kotak and Lula are moot: the US dollar does wield enormous clout. Worse, it is weaponised, especially against countries that fall foul of American interests.

In the last few years, ever since China started to challenge the hegemony of its one time mentor, the debate around the power of the dollar has gained ground. Recent utterances, by Kotak and Lula, only reaffirm these sentiments.

Matters came to a head with the breakout of war between Russia and Ukraine. Part of the sanctions imposed by the United States included shutting down the payment gateways owned by American companies. Further, nearly half of the over $600 billion in foreign exchange reserves owned by Russia have been frozen.

It was a rude reminder about the power of a weaponised dollar. But, is there something the rest of the world can do?

A Reality Check

The rhetoric around the imminent decline of the dollar has gained ground because of some structural shifts that are underway.

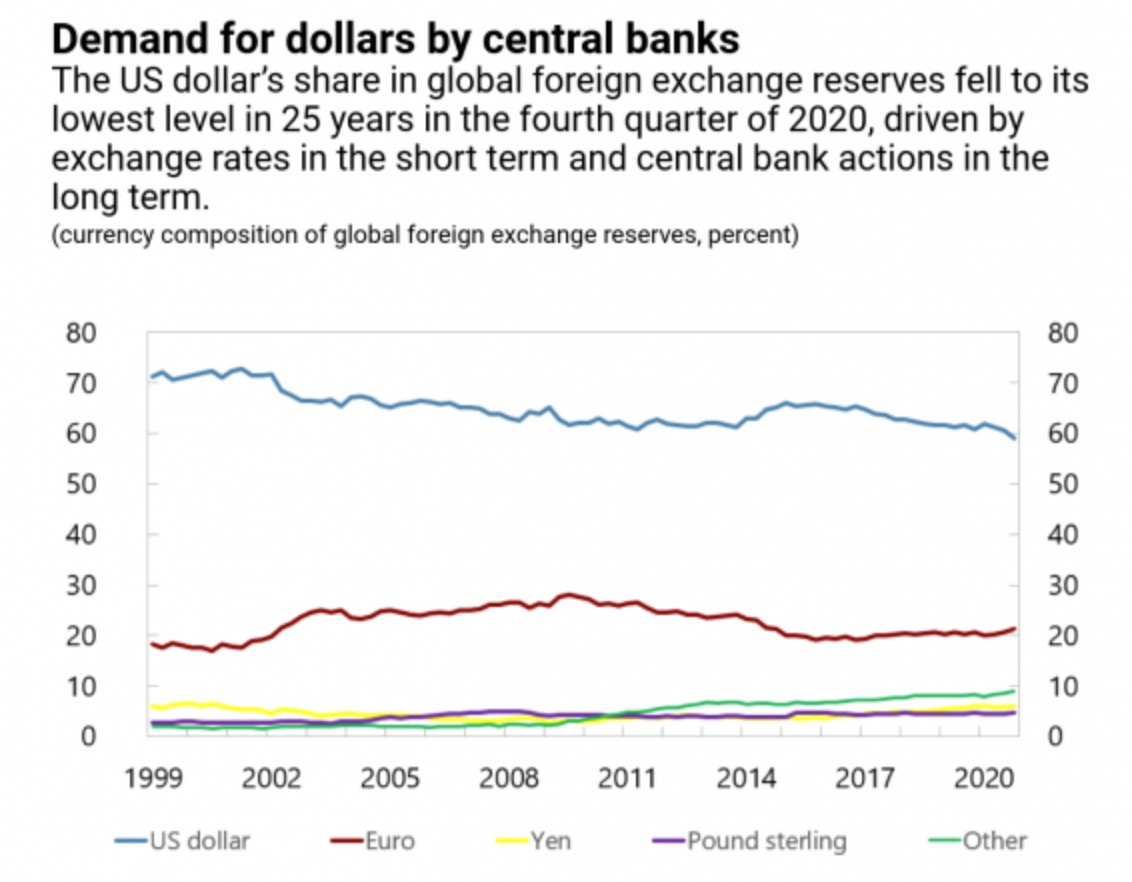

For instance, the share of the US dollar in foreign currency reserves (captured in the graphic above) maintained by central banks of countries, dropped to a 25-year low in the fourth quarter of 2020.

From about 70% in 1999, it has dropped just below 60% in 2020.

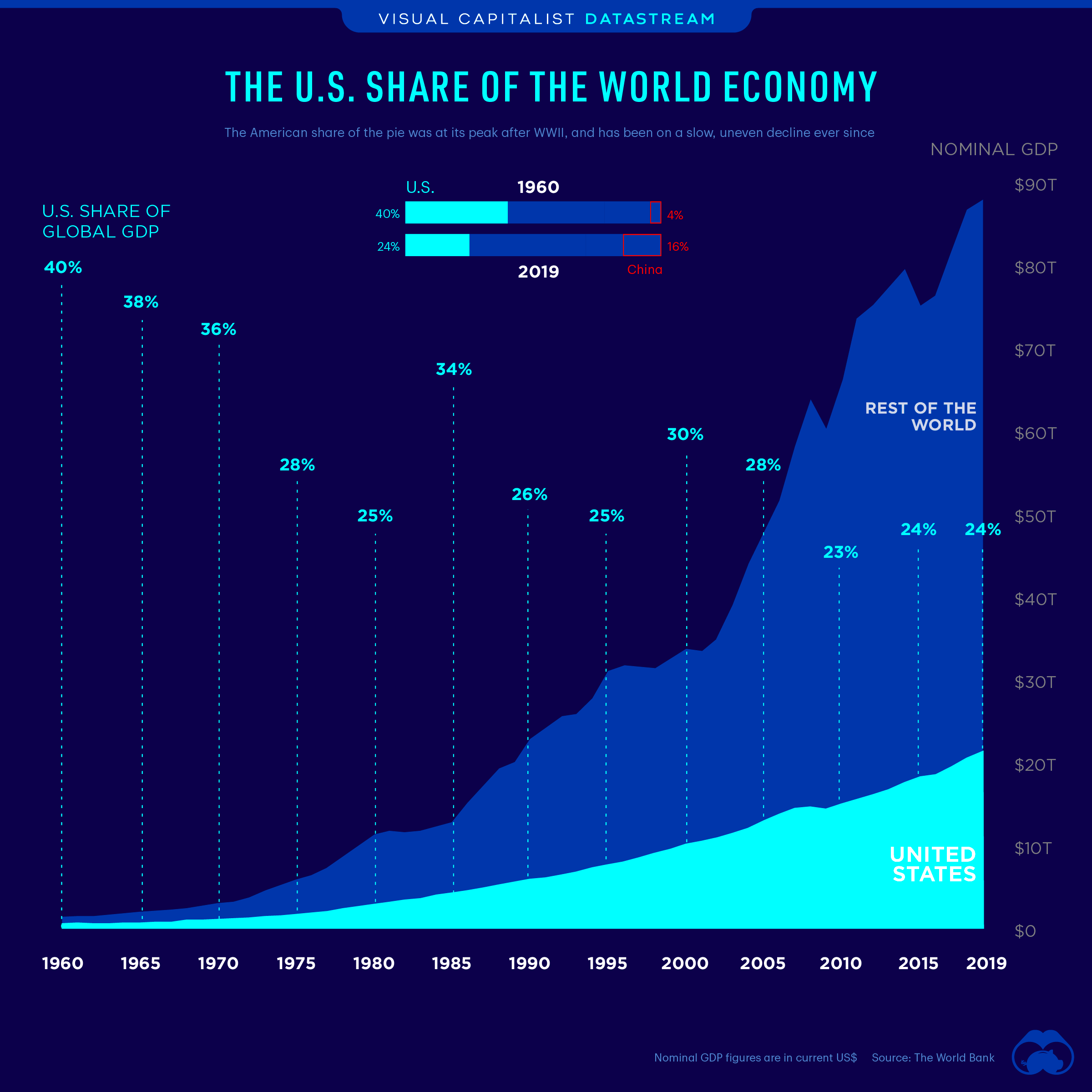

Similarly, the share of the US economy in world output (captured in the graphic above, sourced from Visual Capitalist) declined from 40% in 1960 to 24% in 2019. This is partly due to the fact that the global economic pie has grown with the rise of countries like China.

While all of this is true, talk about revisiting the dollar’s preeminent position looks premature. I am not saying it won’t happen, but to think that this will happen in the near future is a pipe dream.

For starters, the US continues to be the world’s largest economy: $25.46 trillion at the end of 2022.

The nearest challenger is China, with an official claim of $17 trillion—this, as you will see in this week’s interview on StratNews Global (shared below), should be taken with a pinch of salt; in other words the gap is much larger. To provide context, India’s GDP is estimated at $3.5 trillion.

Another bit of reality—despite the shrinking global economic presence of the US—is that 80-90% of global trade transactions continue to be in dollars. Further, the world has racked up over $10 trillion worth of debts denominated in dollars.

Further, the loss in share of the US dollar in the foreign currency reserves (referred to in the first graphic) maintained by foreign banks, has not accrued to other reserve currencies like the Japanese Yen, Pound Sterling or the Euro. Instead, they are being held in currencies like the Swiss Francs, Australian dollar, Canadian dollar and Chinese Renminbi.

Finally, while moving away from the dollar may be desirable, the stark reality is that this is almost inconceivable at the moment. Indeed, if the world did go down this path, then the disruption that would ensue, including geopolitical consequences, would be humongous.

In the final analysis it is clear that reality is not matching the rhetoric against the hegemony of the US dollar. Instead, it seems as though countries are seeking to de-risk their exposures to protect against a weaponised dollar.

This is consistent with the growing love for gold among central banks. Back home in India, beginning 2018, the Reserve Bank of India has grown the country’s gold reserves from 560.3 tonnes to 790.2 tonnes in February this year—an increase of 41.03%.

Another example is the way India has evolved its own payments platform—the Unified Payments Interface powered by the National Payments Corporation of India—as an alternative to the payment gateways owned by US firms like Visa and Mastercard.

But, these are mitigation strategies and not decoupling from the US dollar. For now, the simple truth is that the US dollar will continue its global domination. You may not like it, but you will have to live with it.

Recommended Viewing

Sharing the latest post of Capital Calculus on StratNews Global.

The fault lines between Western nations and China were visible even before the onset of the covid-19 pandemic. In the last three years these differences have worsened as western nations moved to decouple from China—something that is easier said than done given the deep and complex economic linkages.

If this was straining the economy, the pursuit of a zero-covid policy only made a bad situation worse. Undoubtedly all this has begun to take its toll of the Chinese economy—most visible in declining exports.

Yet, counterintuitively, the size of the Chinese economy has grown from around $14 trillion to around $18 trillion in this economically traumatic phase. Clearly, a reality check on the Chinese economy is imperative.

We spoke to Shehzad Qazi, COO, China Beige Book International. China Beige Book is the world’s largest repository of privately accessed data on China. The go-to portal for those seeking an alt-view on the Chinese economy.

In his very forthcoming style, Shehzad pointed out that the Chinese economy was slowing and in the midst of a key pivot. For starters, the years of runaway economic growth are over, even as the shadows of fiscal misadventures lengthen. Do watch the interview for more insights.

Sharing the link below.

Till we meet again next week, stay safe.

Dear Anil,

Very interesting article! After every few years, doubts are raised on whether the US dollar will continue to be the international currency? There have been questions about the stability of American financial system, trouble in some American banks and the ability of the dollar to continue as the medium of global financial and trading system . But we can say with out any doubt that there is no alternative to dollar at present.More than 60% of global foreign exchange reserves are in dollars, close to 50% of global trade is still invoiced in dollars and also the international loans .

Hence the idea of de- dollarization is far fetched at present!!

This change has been contemplated seriously in the last few years and India has made an arrangement with Russia for imports of oil. However, the cheaper oil has made it a lopsided balance of payments with them. INR is not easily convertible and paying Russia in USD will result in US sanctions. So here we can witness both the examples of bilateral trade where the USD has been excluded and also the difficulty, if the import and export do not match. Under the circumstances I feel that gold could be used as the reserve currency, as the international price of bullion could be used for determining the value of gold to be transferred. Both countries would still benefit in such exceptional circumstances. In fact cheaper Russian oil has actually helped to stabilize the Indian economy and has also helped to reduce the international oil prices.