DIALLING TRADE

India is moving swiftly to clinch bilateral deals, signalling a reset in its approach to global trade and its national security paradigm. EPISODE #74

Dear Reader,

A very Happy Monday to you.

Last week a high level delegation from the United Arab Emirates (UAE) led by Abdullah bin Touq Al Marri, minister of Economy, touched down in India. The team was here to flesh out the contours of the newly minted UAE-India Comprehensive Economic Partnership Agreement (CEPA). While the details are still being worked out by both sides, there are some clear signals, especially from India.

The big takeaway is that the UAE bilateral trade deal is the beginning of a new chapter in not just the economic history between the two countries but also a larger reset in India’s approach to global trade.

So this week I explore this trend and unpack the attendant implications of this bold shift in approach by India. Do read and share your feedback.

The cover picture is sourced from Unsplash and taken by Tetiana Shyshkina. Hopefully this will put the spotlight on the ongoing conflict, which is now threatening to snowball into an unprecedented global food crisis.

A big shoutout to Adarsh, Ranjini, Kartik, Vandana, Gautam, Niranjan, Premasundaran, Subash and Preeti for your informed responses, kind appreciation and amplification of last week’s column. Gratitude also to all those who responded on Twitter and Linkedin. Reader participation and amplification is key to growing this newsletter community. And, many thanks to readers who hit the like button😊.

THE BIG BET

Last week a high level delegation from the United Arab Emirates (UAE) led by Abdullah bin Touq Al Marri, minister of Economy, touched down in India. The team engaged in extensive conversations with their Indian counterparts to flesh out the contours of the newly minted UAE-India Comprehensive Economic Partnership Agreement (CEPA).

Significantly, a month earlier, India laid the groundwork for a similar CEPA when it inked an interim deal with Australia on 2 April. The full deal is expected to be clinched later this year.

In a short time India has clinched a CEPA with its third and 20th largest trading partner. And this from a country, handicapped by its poor competitiveness and logistic bottlenecks has historically almost always approached international trade negotiations defensively.

Unlike a Free Trade Agreement (FTA), which focuses primarily on trade in goods, CEPA extends to services, investment, government procurement and is respectful of the regulatory regime in each country. It has strategic connotations too.

Keeping in mind that CEPA is both more comprehensive and ambitious than a Free Trade Agreement (FTA), India is making a bold bet—one in which the traditional crutch of tariffs now has a sunset clause; instead the cutting edge will be India’s competitiveness.

This is a paradigm shift. One in which every economic constituent in the country, including India Inc and the government, will have to play their A-game. Implicitly it suggests that the government is confident that ongoing economic reforms will iron out the kinks, especially with respect to the law, logistics and access to credit, to give Indian entities a level playing field.

To the discerning it will be apparent that the two CEPA deals also coincide with the growing strategic proximity of the two countries. The logic is easy to comprehend. While the UAE provides India a window in West Asia (with access to Africa), Australia is a QUAD (the Quadrilateral Security Dialogue between Australia, Japan, United States and India) partner.

Together these two deals have the potential to spawn a new and powerful trade corridor connecting West Asia to the Indo-Pacific through India.

Finally CEPA is also a tacit recognition that the global multilateral trade is on hold. The western world had progressively undermined the World Trade Organisation, once they realised that nimbler countries like China were getting the better of them. The recent fallout with China only accelerated this process. The CEPA therefore is also an acknowledgement of a new global reality.

Good Morning UAE

Not many may be aware that prior to the signing of the CEPA, UAE was already India’s third largest trading partner (total trade was valued just under $60 billion before covid struck in 2020) and the eighth largest foreign investor ($18 billion). According to the commerce ministry, in the next five years CEPA will expand bilateral trade in goods to $100 billion of services to $15 billion.

The most succinct summation of the CEPA and its implications was made by Biswajit Dhar, one of the finest trade experts in the country and a professor at the Jawaharlal Nehru University. (Full disclosure he is a dear friend and my go-to expert on all matters relating to trade.)

In an opinion piece published in the Hindustan Times, he said:

“The India-UAE CEPA marks a departure from India’s past FTAs in three significant ways.

—The negotiations were concluded in less than three months after being initiated in end-September 2021. This is remarkable given that FTA negotiations involving India have generally been long drawn.

—The agreement covers the widest array of subjects, including digital economy and government procurement, which have never been included in any bilateral trade agreement that India has negotiated thus far.

—Market opening commitments that India has accepted in this agreement, especially in the goods sector, is the most extensive of any FTA signed by the country.”

If you wish to read the entire piece (highly recommended) please click this link.

The Edge

It is evident then that India can no longer afford the existing attitude of business as usual. The government has thrown down the gauntlet. Retreat is no longer an option, suggesting that you either perform or perish.

And in this India Inc will have to shed its diffidence and bat from the front. The country’s chief economic advisor Anantha Nageswaran, in his incisive style, laid out the to-do agenda for India Inc.

In an opinion piece published in Mint, he said:

“The Indian private corporate sector has several advantages as it enters a new decade. Its balance sheets are healthier than before. Its profitability is high while Indian corporate tax rates and real borrowing costs are low.

Space is opening up for India to exploit avenues created by myopic policies pursued by some other nations. It is time for Indian businesses to aim bigger and lengthen their horizon.

The focus has to be on win-win: pay small suppliers on time, help the pie of prosperity grow bigger, and focus on competitiveness gains through investment in research and technology, rather than through a weaker currency and tariff protection.”

The Odds

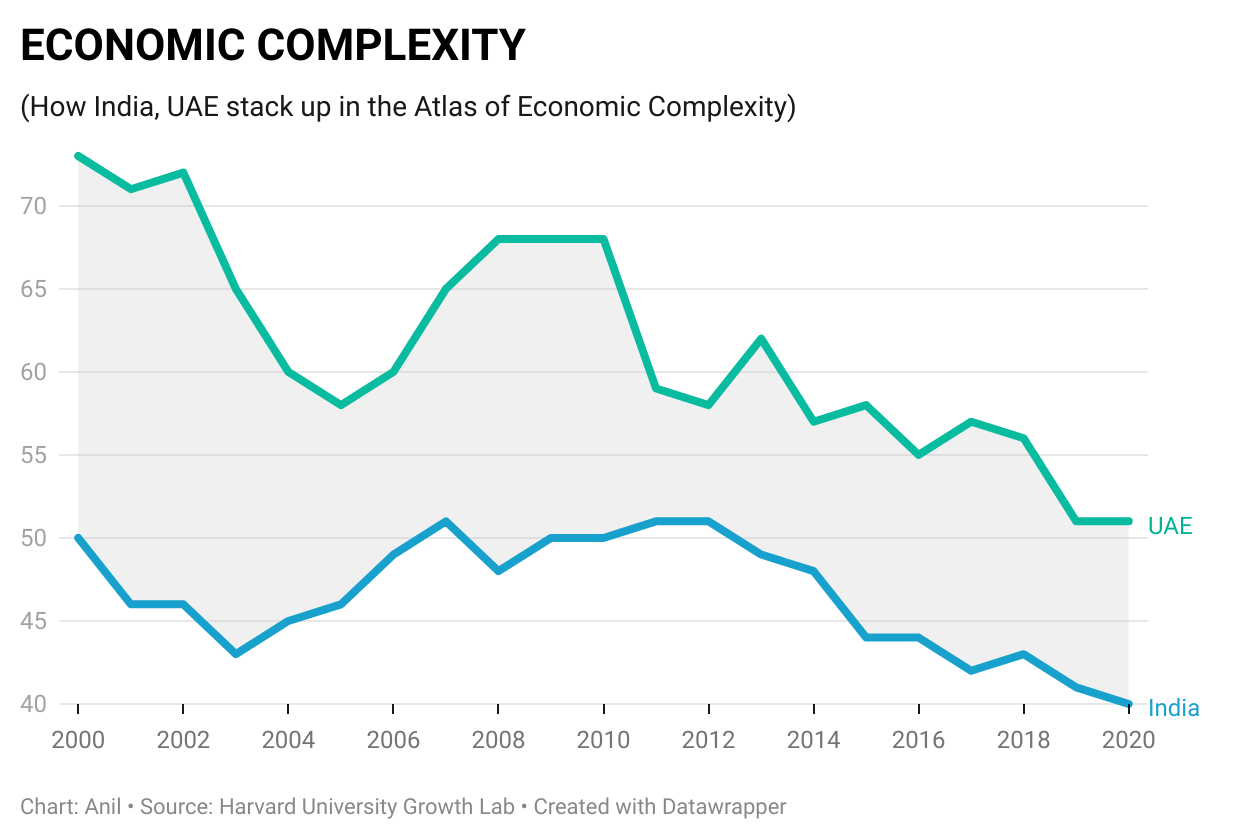

Undoubtedly the odds are stacked against India Inc. And this is particularly apparent if we peruse the economic complexity of India and measure its rankings against other countries.

The Atlas of Economic Complexity has been developed at the Harvard Kennedy School of Government. It is premised on the belief that you cannot have economic development without accumulation of productive knowledge and increasing its deployment in complex industries. The country rankings in the Atlas capture a country’s current capacity of productive knowledge.

India does not figure in the top 20 countries in the latest rankings.

If this does not serve as a wake-up call then this should: Unlike say China, India’s progression in the ranking table is far from desirable.

The only saving grace is that India is better off than the UAE. At the same time it should be noted that the UAE is rapidly catching up—the gap between the two worms in the graphic above have shrunk in the last two decades.

However, the Atlas of Economic Complexity report on India believes it has the potential.

“India ranks as the 43rd most complex country in the Economic Complexity Index (ECI) ranking. Compared to a decade prior, India's economy has become more complex, improving 12 positions in the ECI ranking.

India's improving complexity has been driven by diversifying its exports.

Moving forward, India is positioned to take advantage of many opportunities to diversify its production using its existing knowhow.

India is more complex than expected for its income level. As a result, its economy is projected to grow rapidly. The Growth Lab's 2029 Growth Projections foresee growth in India of 5.1% annually over the coming decade, ranking in the top quartile of countries globally.”

Clearly the government is convinced that India is poised to realise this potential. It has demonstrated its chutzpah by inking two CEPAs, with the promise that several more will be clinched by the end of this calendar year.

A bold bet indeed. But now to walk the talk.

Recommended Reading

On 30 April India did a soft launch of the Open Network for Digital Commerce (ONDC). Another daring bet, but this time to disrupt the business of trade.

A week after the launch I wrote about it in my monthly column for the Economic Times. Sharing a screenshot below.

If you wish to read the piece online please click this link.

As a regular reader you may find overlaps with my previous newsletter post on ONDC. Apologies.

Till we meet again next week. Stay safe.

Dear Anil,

Excellent analysis of a topic not many have written about!! Full of knowledge and interesting Statistics!!

Super mine of informed information.

Way to go, Anil