BRIDGING INDIA'S GENDER GAP

A convergence of circumstances is enabling gender parity in India, albeit slowly. EPISODE #52

Dear Reader,

A very Happy Monday to you.

Little over a fortnight ago, the government released the fifth round of the National Family Health Survey (NFHS-5). It threw up a pleasant surprise: The sex ratio for the total population went up from 991 females (per 1,000 males) in 2015-16 to 1,020 in 2019-21. Similarly, in the same period, the same female-male sex ratio at birth improved from 919 to 929. Importantly improvements were observed in the traditionally laggard states of Haryana, Punjab and Uttar Pradesh.

Separately, the union finance ministry informed Parliament that of the 440 million Jan Dhan (or no frills) bank account holders more than one in two were women.

Coincidentally, last weekend I published a new feature in Khaleej Times on how the business of personal finance is witnessing a makeover: the burial of one-size-fits all approach. A convergence of circumstances, especially of growing aspirations among women and the rise of FinTech, is now making a business case for creating products tailored to the unique needs of women.

Connect the dots and what we see is progress on the vexing issue of gender parity. Yes, the pace is far from satisfactory. But the good news is that change is in the air. So this week I focus on the subject of gender parity.

This week’s cover picture is from Unsplash and taken by Srimathi Jayaprakash. Thank you Srimathi.

A big shoutout to Abhijit, Gautam, Premasundaran and Vandana for your informed responses, appreciation and amplification for last week’s column. Gratitude also to all those who responded on Twitter and Linkedin. Reader participation and amplification is key to growing this newsletter community. And, many thanks to readers who hit the like button; Ashish Jain are you listening? 😊.

If you are not already a subscriber, please do sign up and spread the word.

THE GENDER STORY

As mentioned above the union government released the fifth round of the results of the National Family Health Survey (NFHS-5). Indeed it threw up a pleasant surprise: The sex ratio for the total population went up from 991 females (per 1,000 males) in 2015-16 to 1,020 in 2019-21. Similarly, in the same period, the sex ratio at birth improved from 919 to 929.

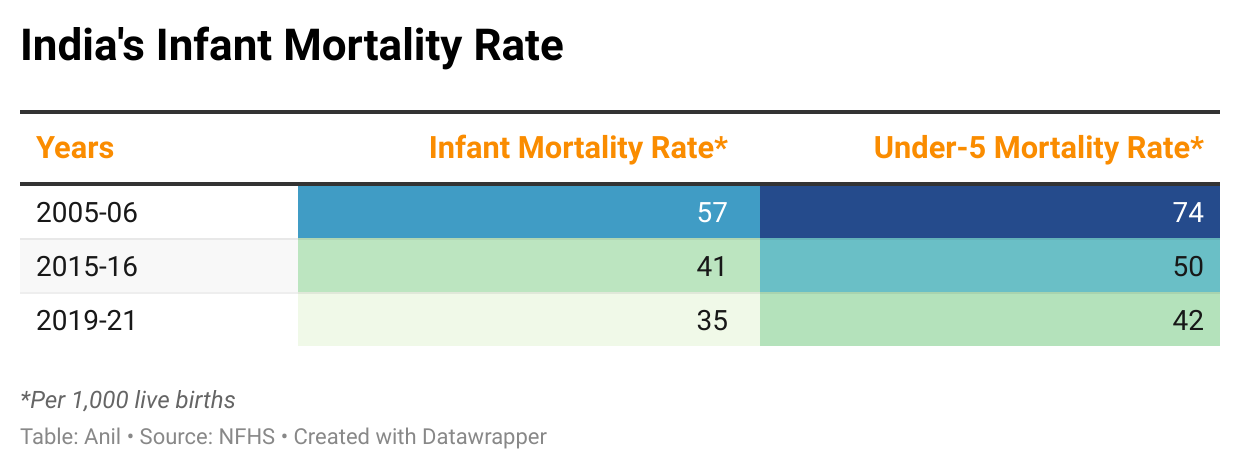

The bad news though is that the numbers also chronicle the astonishing tale of public policy neglect and failure. And that the real progress has commenced only after the turn of this Millennium. Sharing two charts, also sourced from the NFHS, to argue my case of this abject neglect.

It is difficult to process the startling fact that till as recent as 2005-06, the mortality rate for children under-five years was 74 per 1,000 live births. Yes, while it has declined since it is still at 42. In comparison in the United States this proportion is 5.6, while in Bangladesh it is 30.8.

Wait till you peruse the country’s literacy rates. I recall my Mexican batchmate in an international programme in 2000-01 telling me that her country was 100% literate. And I had to shamefacedly share that at that point of time the literacy rate for India was 65% and that just about one in two women in India were literate.

Tragically, 20 years later India is still playing catch-up with Mexico. I am not sure as to how I will explain the glacial pace of progress to my friend if our paths were to cross again.

And what bothers me more is that we still have politicians in India who swear by status quo; worse, people are willing to vote for them!

There is one bit of good news though in the latest round of NFHS: the gap between male and female literacy has shrunk. But let us not forget even at this level little over one in four women in India are illiterate—the proportion among males is just under a fifth. And this 75 years after Independence.

The thing about India is that it is a story of change at multiple speeds. While the overall story is still sadly a work in progress—in terms of getting basic development parameters right—there are several segments where the power of technology is expediting this makeover.

The X Factor

And one such empowerment is with respect to banking and personal finance services for women. As disclosed in the introductory letter 55% of the 440 million Jan Dhan accounts for the poor are held by women. Yes, many may not be operable. But that does not mean they won’t be in the future. And at that point of time there will be one challenge less.

Simultaneously, a constellation of circumstances—the rapid adoption of FinTech and the growing aspirations among women—is forcing change in the business of personal finance. Probably for the first time ever the strategy of one size fits all is being abandoned and the savings and investment needs of women are being aligned to their often unique on-off work trajectories.

I did a fairly detailed feature on this for Khaleej Times, the Dubai-based daily. Sharing a screen grab from the paper. If you wish to read the story please click here.

As I argue in the feature, women despite accounting for half the population, are a very underserved community in India. Guesstimates peg the size of female investors at around 1%. The good news is that a mindset reset is underway. The story of Jan Dhan accounts tells us that this change is extending beyond the four metros.

Similarly the story also busts some popular myths, one of them being that women are risk averse. As several people interviewed for the story pointed out women are “risk aware”. And which leads into the thesis put out by LouAnn Lofton in 2011 arguing that women make for better investors. In fact she audaciously titled the book: Warren Buffet Invests Like A Girl…And Why You Should Too. If you wish to read the book (highly recommended) please click here.

In the final analysis it is apparent that change is in the air. But overcoming a legacy deficit of this magnitude is excruciatingly slow. But then who said transformative change is easy.

Recommended Reading

Researching my Khaleej Times feature I spoke to several people. One of them was Shinjini Kumar, co-founder of SALT (mysaltapp), a platform for women buying financial products.

I could not use most of her interview for the story. But felt it is a brilliant read and hence the share. These are edited excerpts from the telephonic/email interview with her.

Q: Why do we need instruments specifically for women?

A: One is that financial services overall have selection and elimination criteria across products. There are eligibility conditions, ticket sizes, fee structures, AML questionnaires etc. So, there is a lot of discretion to the supply side. And who determines and implements these eligibility and gating conditions? It is largely the male, elite world. As a result the minorities, including women, tend to get excluded.

Second, lifestyle choices and constraints of women are very different from men. For the same job, women get paid less; more women take career breaks for family reasons. More women drop out of the workforce and often don’t come back. Also more women find it hard to start a new business, access credit or VC funding. Fewer women own assets for providing collateral.

This influences your choices, usage and consumption of financial products. Because you are different, your lifestyle is different, source of money is different, quantity of money is different, your allocation of investments, your need for saving or insurance are likely to be different too. Hence the need for different products and solutions.

Q: Do platforms dedicated for women make this easier?

A: I do feel it is required for women to be building for women. It is almost as if the woman customer of finance is invisible. So you see the most high profile women customers and you conclude that everyone can ‘reach up’ and access. In addition, perception of women in poor income strata is the stereotype of the hard working, saving, loan paying women, which is not the wrong stereotype, but is a very limiting one. It is very hard to come across detailed gender data and data cuts. As a result it is hard to build personas.

It takes a lot more motivation, and when you are operating in the otherwise lucrative financial services space, it is easy to go for the client who is already visible and ready. So being a women building for women is important for that extra motivation.

There is no incentive for the existing financial system to collate this information on women. Rather than finding that 5 million population you can always grow your business from the 20 million customers who are ready to come to you—which may include over 80% men as is normally the case. So there is a business case for a platform for women.

I don’t wish to use the word niche, because with half the population being women it is certainly not niche. But differentiation in approach, yes.

Q: What will it take to map the risk profile of women and customise products for them? Is the market ready?

A: Everybody wants to give money to someone they trust and everyone wants return on their investment. Since it is not always possible to ensure complete safety of the capital and return, there is a concept of risk that gets into it. Principally, the concept of risk should apply across the board in a similar manner. But it does not. Because again, risk models are built on historic data and has fewer data points for women.

So, it is very interesting to challenge the theory that women are risk averse. I am not sure whether it is the cause or the effect because sales people are actively told not to sell risky products. We have to ask if the supply side has indeed done a good enough job of explaining risks and building models based on inclusive data. It is so much easier to simply segregate and discriminate.

Q: The design of products are prejudiced by gender, right? How do you fix this?

A: It is not even the prejudice of gender. It is the legacy of finance; how financial products were created for consumers. It made some assumptions—like people will earn monthly salaries, will need cars to commute to work and own a house. Now we are living in times where people may prefer to take an Uber, live in an AirBnb and may not work long term jobs. So it is not gender prejudice.

Instead it is a matter of legacy that has defined our credit models and other financial products. So these assumptions are up for disruption because those lifestyles have changed or have disappeared. In the context of women those were always different, just that no one was paying attention to it. You can’t afford to ignore them anymore as the young people no longer live that lifestyle.

This in turn means that if you have to sell finance to them you will have to change. We are approaching it from gender perspective because we see this as the largest cohort facing this problem.

Till we meet again next week. Stay safe.

Anil very motivating article. Just sharing, for last 10years NGO CHAUPAL is giving microfinance to the poorest women to make them self sufficient. By offering 20k we ensure minimum help for 1year at 5% pa administrative expense only. And the most brilliant aspect is 98.9% repayments by women. Comparison Men were financed e rickshaws and the repayments are woefully woefully atrocious, only 13%. Starting a project shortly whereby poor women will be trained to drive and maintain garbage erickshaws in a district in Odisha.

Dear Anil,

A very well timed article as all newspapers are full of debate and discussions on govts proposals to raise legal age of marriage for women to 21years.A step in right direction I would say as it is required to lower MMR, I MR , improvement in nutritional levels and sex ratio.

WOMEN comprise around 49% of Indian population but women still comprise less than 15% of loksabha..The bill for 33% reservation of seats in parliament for women has been hanging for 25 years. Focusing on women could modernize Indias politics.Every election now is showing increasing involvement of women, awareness of women's safety, economic well being is the need of the hour if India has to become a developed nation.