A GLOBAL RUPEE

A GLOBAL RUPEE

By allowing invoicing of trade in rupees the Reserve Bank of India has moved the country a step closer to internationalising the rupee. EPISODE #82

Dear Reader,

A very Happy Monday to you.

Last week the Reserve Bank of India (RBI) permitted rupee invoicing and payments for both exports and imports. The immediate assumption, voiced by several arm chair analysts, was that this was being done to circumvent global sanctions against Russia and allow India to pay for its imports.

While this may be one instance of the use of this facility it is not the only one. The larger intent is to internationalise the rupee.

Indeed this is not the first step. If anything the latest move is among a series of steady moves undertaken by India over the last decade to make the Indian rupee part of the global trade lexicon—similar to other hard currencies like the Swiss Franc, Japanese Yen, British Pound and so on.

So this week I explore the idea of a global rupee and the attendant implications. Do read and share your feedback.

The cover picture is sourced from Unsplash and taken by Divyanshi Verma. Thank you Divyanshi.

A big shoutout to Niranjan, Vandana, Gautam, Kapil, Premasundaran and Aashish for your informed responses, kind appreciation and amplification of last week’s column. Gratitude also to all those who responded on Twitter and Linkedin. Reader participation and amplification is key to growing this newsletter community. And, many thanks to readers who hit the like button😊.

RUPEENOMICS

As mentioned in my introductory note, last week the Reserve Bank of India (RBI) tweaked its stringent foreign currency rules and allowed both exporters and importers to invoice and pay in the Indian rupee.

Actual fact is that rupee trade is negligible at present. As a result, the move has not caused any ripples. Except for the lot which is vocally making a case that this is all a grand conspiracy to work around global sanctions against Russia—by paying for its trade in rupees India will be able to avoid using foreign banks who otherwise broker dollar denominated trade deals.

Such reactionary responses often see events in isolation.

By ignoring history what has been overlooked is that the move by RBI is not random. Neither is it a culminating step. It is part of a calibrated sequencing of steps that have been rolled out over the last decade and more, designed to both test global waters and ready the Indian economy for a globalised rupee.

The trigger for this rethink was the global crisis in 2008 set off by high risk subprime bonds going into default. The resulting global meltdown exposed the vulnerability of individual countries to the vagaries of a predominantly dollar denominated trade. China, which by then had acquired sufficient heft to challenge US hegemony, launched the Renminbi as an alternative currency.

Undoubtedly it was a terrific idea. Something which however needed a major reset in the prevailing business and economic mindset of India. In short the Indian economy would have to be retooled to pass the stress test that will come with an internationalised rupee.

And such a structural reordering can only be achieved incrementally that is carefully sequenced. The internationalising of the rupee is evolutionary in nature and therefore requires building blocks that are carefully crafted and placed. It cannot be achieved overnight.

An Identity

Till a decade ago India had not ascribed a unique symbol to the rupee. The then Congress-led United Progressive Alliance (UPA) initiated this project by crowdsourcing symbols.

Presenting the 2010-11 Union Budget the then finance minister, Pranab Mukherjee, said:

“In the ensuing year, we intend to formalise a symbol for the Indian rupee, which reflects and captures the Indian ethos and culture.”

And then added:

“With this, the Indian rupee will join the select club of currencies such as the US dollar, British pound sterling, Euro and Japanese yen that have a clear distinguishing identity.”

The winning design was submitted by D Udaya Kumar. It was an amalgamation of the Devanagari letter ‘Ra’ and the Roman capital letter ‘R’. The note explaining the design philosophy said:

“The letters are derived from the word Rupiah in Hindi and Rupees in English—both denote the currency of India. The derivation of letters from these words conveys the association of the symbol with currency rupee.

The symbol straightforwardly communicates the message of currency for both Indian and foreign nationals. In other words, a direct relationship is established between the symbol and the rupee.”

Establishing Credibility

Ahead of this search for an identity, India had begun to gradually loosen the controls on foreign currency and trade. Most of the 1990s was spent in bringing down the peak tariffs, which at one time topped 400%.

As the economy slowly limped its way out of the 1991 crisis, it also began to revisit the controls on the balance of payments. It began with the current account—which captures the value of the goods, services and invisibles (like money transfers by expats or payment of royalties) traded by India.

As a result, by the turn of the Millennium the rupee was fully convertible on the current account. Logically, the attention then shifted to undertaking another round of calibrated liberalisation on the capital account of balance of payments—for instance at the moment foreign portfolio investors can move their money in and out (as has been happening for the last six months and more) freely.

What these moves did was to allow for a market determined value of the rupee. It is well accepted that market determined economics stokes competitiveness. Prior to 1991 it was fixed by the RBI. Two decades into this new regime, the economy as well as its constituents had retooled themselves to the liberalised environment.

More importantly it started to gradually establish the credibility of the Indian rupee in commercial transactions.

Simultaneously, work had begun to introduce transparency in monetary policy formulation that enabled a flexible inflation target. Again this can’t be seen in isolation. This conversation had already begun in RBI, during the tenure of the UPA.

It was the Bharatiya Janata Party (BJP)-led National Democratic Alliance (NDA) which took this to the logical conclusion and set up the Monetary Policy Committee (which included external members) in 2016 and the guardrails for what is described in official lexicon as flexible inflation targeting (FIT).

A Global Rupee

Keeping this backdrop—the macroeconomic bulwark required for a global rupee—in mind let us rewind the clock to the 2008 global economic crisis. Immediately thereafter RBI began internal conversations about taking the logical step of internationalising the rupee.

Addressing the Bank for International Settlements in 2009, soon after the subprime crisis, the then deputy governor of RBI, Shyamala Gopinath, formally disclosed that the idea was under consideration.

“Internationalisation of a currency is a policy matter and depends upon the broader economic objectives of the country.”

And then signalled that it was a work in progress:

“Recent global developments have considerably heightened the uncertainty surrounding the outlook on capital flows to India, complicating the conduct of monetary and liquidity management.

In such scenario, cautious movement in terms of internationalising the currency is in order. There are indications to believe that Indian rupee is gaining acceptability in other countries. However the size of the country in terms of GDP, volume of trade as also the turnover in the foreign exchange market when compared with global dimensions, is small.

The Indian rupee is rarely being used for invoicing of international trade. Therefore, internationalisation of the rupee is still a distant objective of policy makers in India.”

A year later, a research note generated by RBI revisited the idea in the context of the attempts to internationalise the Chinese Renminbi. Very candidly, the paper published in 2010 admitted that the Chinese economy was much better placed to attempt it.

In the Indian context the study said:

“The Indian rupee is rarely being used for invoicing of international trade. All the necessary preconditions need to be in place before India could proceed further on the issue of internationalisation of the rupee.

In view of this, India needs to proactively take steps to increase the role of the Indian rupee in the region (sub-continent).”

Since then, as India gradually began to acquire economic heft and put in place transparent rules for fiscal and monetary management, RBI has frequently revisited the idea of internationalising the rupee.

In fact the tone of its public utterances is acquiring certitude off late. The RBI Currency and Finance (2020-21) said as much:

“Looking ahead, the emergence of INR as an international currency appears inevitable.”

But then added that this transition has its benefits but comes with a tab:

“While greater internationalisation of the INR can lower transaction costs of cross-border trade and investment operations by mitigating exchange rate risk, it can also complicate the conduct of monetary policy. Internationalisation of a currency makes the simultaneous pursuit of exchange rate stability and a domestically oriented monetary policy more challenging, unless supported by large and deep domestic financial markets that could effectively absorb external shocks.”

And then added that there is a necessary condition, which is non-negotiable.

“Besides deep and sophisticated financial markets, the most important pre-requisite for internationalisation of a currency is price stability. Inflation, higher than the world average, undermines the use of a currency as an international medium of exchange and a store of value and can restrict the role of such an economy in global value chains.

While high inflation disincentivises cross- border trade and investment by enhancing the cost of acquiring information for pricing, stable prices build confidence of international investors in the domestic currency. In India, the primary focus of FIT (Flexible Inflation Targeting) on price stability augurs well for further liberalisation of the capital account and internationalisation of the INR.”

Stress Test Capability

The good news is that slowly and steadily the building blocks for internationalising the rupee are coming into place.

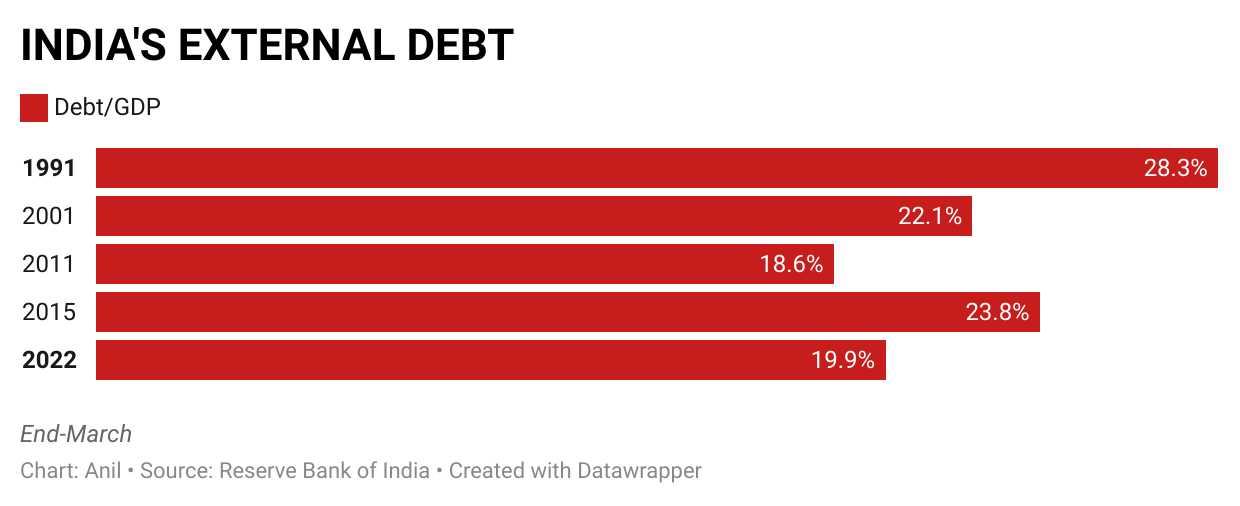

Of particular comfort is the decreasing vulnerability of the external sector—especially when compared to the meltdown that India experienced in 1991. One such metric is the size of the external debt.

Yes, the stock of external debt has grown. But so has the country’s economy—and the external debt is always measured in proportion to the GDP. The graphic below shows that it is not at alarming levels at present.

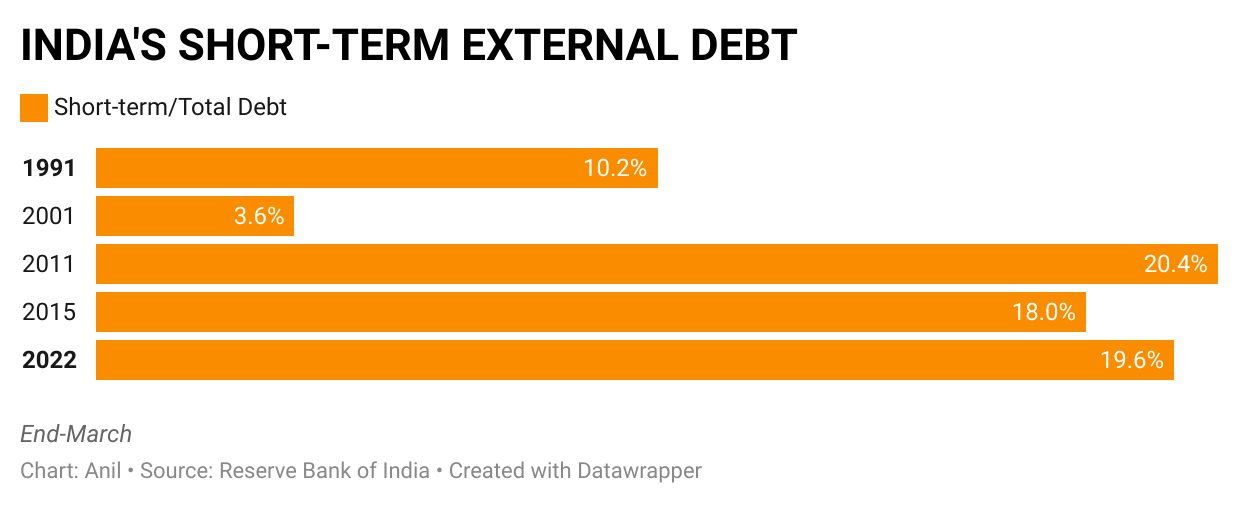

Another metric is the size of the country’s short-term external debt, which in inclement circumstances, can be a potential problem.

The thumb rule is that borrowing should not fund consumption. Presumably Indian economic entities are borrowing to finance its investments. In that case the present levels of outstanding short-term debt is not a cause for worry.

In turn, what this external sector cushion is doing is that it allows greater independence to monetary policy. The resulting macroeconomic stability is an important sequence in internationalising the rupee.

In the final analysis it is clear that India is slowly and steadily moving towards a global rupee. The decision by RBI to allow rupee invoicing was only a reaffirmation of this determination.

Recommended Reading

Last week the National Aeronautics and Space Administration (NASA), the agency of the US federal government responsible for their civil space initiatives, released the first set of pictures from the James Webb Space Telescope.

Located 1.5 million km from earth this satellite is able to look even further than what has been achieved by previous space-based telescopes. It will dramatically push the boundaries of human knowledge, particularly about the formation of the first galaxies. Looking into our past as it were. Pardon me if this sounds like SciFi.

On Saturday the Economic Times ran a super piece unpacking this ambitious endeavour by Dipankar Bhattacharya, a professor of astrophysics at Ashoka University.

It is both pithy and informative. In short a must read. I am sharing a screenshot of the piece below as a teaser.

If indeed it has your attention please click this link.

Till we meet again next week. Stay safe.

Excellent insights. Global Rupee- in true sense- is few decades away. Government/ RBI will lose a critical policy lever if we make it fully convertible. Selected INR bi-lateral trade have happened in the past too. Freely convertible is way off. But we need to start moving in that direction by RBI.

Super article Anil and what a proud moment it will be if l for one could do my Invoices in INR. Will surely get there if not in the immediate future as initiating a process is the first step in the right direction. Cheers !!!